ISG Provider Lens™ Public Cloud - Solutions & Services - U.S. 2020 - Managed Public Cloud Services for Midmarket

$2499

In the last four quarters, public cloud adoption among the enterprise community in the U.S. has grown drastically. Enterprise demand has now shifted toward more of an as-a-service model, where the preference is for applications based on software as a service, pushing traditional providers and software vendors such as ERP companies to move their packaged applications to run in the cloud. One of the major reason enterprises accelerated their cloud adoption is the COVID-19 pandemic. The COVID-19 crisis has had a major impact in how everyone works. Many organizations wanted to rapidly move their employees to a workfrom-home model, which required significant changes in their application and infrastructure landscapes. Traditional retail, travel and aviation are just a few of the industries that were severely impacted.

Many U.S. workers have been following social distancing norms and working from home for an extended period that started in March and continued throughout September. This has led to a massive rise in online shopping for almost everything, which has changed the business requirements to support work from home, increasing the overall cloud services demand. In addition, most large events — including trade shows, sporting events and festivals — have gone virtual this year. Cloud infrastructure is an ideal ecosystem for this because it provides the agility and scalability required to provide a better customer experience. Virtual business meetings are the new norm, which has often led to deals getting closed much faster. Almost all service providers reported non-stop service delivery, and some have exceeded their planned revenues advance with record-breaking growth, especially IaaS and PaaS providers.

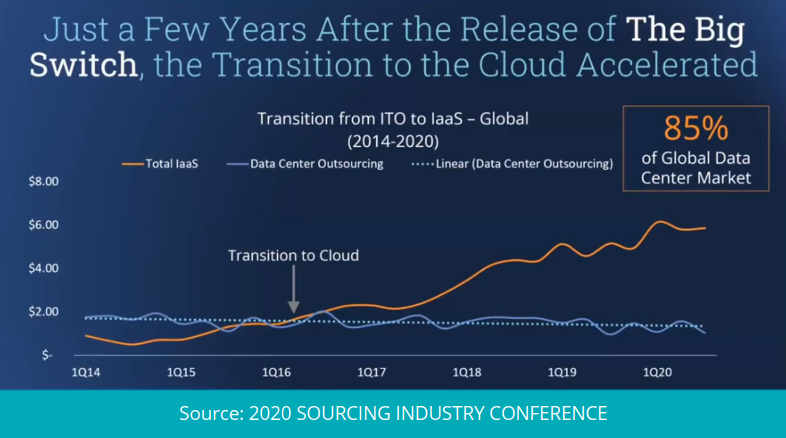

In the recent ISG Index™ call (3Q20), we saw that the global ‘as-a-service’ market grew by 10.5% when compared to the same time last year, within which the IaaS market grew by 14% and SaaS by 2%. The major contributor to this increase was the growth of the hyperscalers, due to accelerated cloud adoption during the pandemic. ISG believes the IT spending will continue to grow and will be mainly driven by IaaS and cloud management providers. Although the traditional managed services business has remained flat across the globe in recent years, the as-a-service market has grown at 20% CAGR, and is more than 50% of the overall outsourcing market. With public cloud infrastructure getting commoditized, enterprises have been adopting cloud technology in their digital journeys, which corroborates the steady growth of IaaS since the last five years.

Cloud-native focused transformation: Previously, there was high demand for lift-and-shift transitions as enterprises just wanted to move their applications to the public cloud. This approach later led to either refactoring or re-architecting the workload so that it performed better, which in turn raised costs. The irony was that enterprise moved to the cloud to save costs, but in the end, had to shell out more money to right-fit the application on the public cloud. Public cloud transformation engagements have now become more meaningful, as the trend has changed to moving the application to the public cloud in a cloud native way, which is mainly driven by the service provider community. Going cloud-native is now a big part of migrating workloads through recoding or re-architecting the application. Container technology and microservices have enabled enterprises to take full advantage of the flexibility and agility the public cloud architecture provides. Several other factors such as leveraging AI/ML and cognitive capabilities for data analysis are also driving enterprises to transform their applications and migrate to a public cloud

environment. ISG also sees a strong demand in transforming legacy applications, which involves completely re-architecting or recoding workloads and moving from COBOL to Java-based applications, which work seamlessly on public cloud infrastructure.

Vertical-specific offerings bolstered by competencies: Service provider partnerships with hyperscalers have become even more important. Along with having a top-tier partnership level, service providers are also rapidly acquiring competency certifications from hyperscalers, which are like prized possessions or trophies. It’s a seal of approval from the public cloud provider that the service provider has achieved expert knowledge in transformation in a particular domain or technology. This helps service providers instill confidence in their prospective clients when they are selling their cloud transformation services. Service providers are also developing industry-specific specialized transformation capabilities to cater to particular verticals, including adhering to their industry compliance and guidelines.

Multi-cloud is the new norm: Applications work differently on different public cloud platforms, and each one of them has certain exclusive capabilities and expertise. For example, AWS offers a broad compute portfolio from basic to high compute requirements for any application development or management. Microsoft Windows and its ancillary product suite are easiest to migrate on Microsoft Azure platform. And Google Cloud Platform (GCP) offers the ideal infrastructure for big data analytics leveraging AI/ML technologies and high graphical and compute-intensive workloads. We have observed that hyperscalers are now being treated as a partner rather than just another infrastructure provider. Enterprises and service provider communities now understand the pros and cons of each hyperscaler and are moving their workloads accordingly. In addition, they do not want to get stuck with one provider because it hinders innovation and sometimes results in high costs. Many enterprise customers have already started to use two or more hyperscalers for different applications, and ISG believes that this trend is going to scale up considerably. But there is a downside to this setup. Several enterprises have mentioned that they find infrastructure orchestration has become difficult because of the several moving parts and the complexity of managing a hybrid multi-cloud environment. To help counter this problem, several service providers and vendors have developed robust cloud management platforms (CMPs), and enterprises are now adopting and using these tools to make their lives easier. Other challenges that enterprises should be aware of with a multi-cloud environment include vendor lock-in by the public cloud provider and the need for interoperability between two or more public cloud providers.

Enhanced managed services: The managed public cloud ecosystem has been growing at a faster rate as overall cloud adoption rises. Enterprises need a helping hand because they are finding it difficult to manage the hybrid and multi-cloud infrastructure. The focus is mainly on cost optimization and moving enterprise resources to core activities rather than on cloud infrastructure management. Also, as the world adapts to working from home, it has become imperative for enterprises to outsource their cloud management and focus on building and innovating new solutions for their clients. Service providers are using DevOps and infrastructure-as-code (IaC) practices as well as artificial intelligence-led automation with out-of-the box API integration capabilities to manage cloud infrastructures efficiently. Automation is still a big part of cloud operations management and is being leveraged along with intelligent DevOps practice for remediation and self-healing capabilities that offer better user experience. Partnerships with hyperscale providers have moved to a strategic level where the vendor and provider work together to develop new solutions and have a joint go-to-market strategy.

Growing demand for cloud GRC services: Enterprises want to move to cloud environments quickly, and as cloud infrastructure landscape is getting complex and intertwined day by day, which may cause several security flaws leading to client data exposed in wrong hands. Some prominent challenges enterprises face while engaging into a cloud transformation are lack of integration among various systems in the organization, vendor/provider management, of integrated risk reporting and financial impact. All these are addressed by governance, risk management and compliance (GRC) service providers. ISG is seeing an increase in demand for integrated solutions of GRC services to help manage cloud transformation engagements in a secure manner. GRC providers have developed robust frameworks that take regulatory, legal, business, and risk environments into account for risk management and follow a “secure by design” methodology.

Rising demand of IaaS and PaaS: Almost all public cloud providers have seen an increase in their business due to the sudden spike in demand for using cloud services and also due to enterprises preferring a multi-cloud setup rather than sticking to a single cloud provider. AWS has a first-mover advantage and has been entrenched in the public cloud infrastructure domain for over a decade. Microsoft Azure offerings are now getting more traction, especially with large enterprises that have legacy Microsoft dependencies such as Office 365 and Windows integration. which makes Azure a popular choice. Azure is catching up fast and is closer to AWS than ever before. Google, too, is catching up and has increased its market reach as several customers prefer GCP for specific use cases such as analytics, big data, and large compute and graphics-intensive workloads.

HANA is the new SAP way: In the last few years, enterprises had plans to move their SAP workloads to a cloud environment, but it was not a high priority. Due to the pandemic, enterprises have accelerated their plans. The overall impression of moving to SAP HANA is positive because it brings several benefits like improved performance and efficiency over legacy systems, better setup for faster innovation, optimizing of existing business processes, faster access to analytics, easier to deliver data, elimination of customization and removal of unnecessary codes. But there have been some pain points experienced during implementation of SAP HANA. These include it being more complex than expected, a difficulty in integration with third-party systems and products, a lack of skilled staff to complete the project, software defects, integration with other SAP solutions, the need to clean up custom code and unanticipated costs.

Enterprises need to choose a public cloud infrastructure provider to host their HANA workloads very wisely, considering factors like its data center proximity, long-term pricing and discounts, and the flexibility to move to another vendor. Hosting SAP HANA on public cloud infrastructure requires knowledge of complexities involved in the migration process and then in operations. Providers must have a clear strategy and structured approach to handling SAP S/4HANA workloads and large-scale HANA databases. Leading cloud infrastructure providers of HANA services are coping up with fast-paced market developments, which include many ancillary cloud services. Such services include supporting infrastructure for other SAP offerings, cost analysis and related operational analysis, provisioning and setup of the technical infrastructure, and go-live and operations support. Deployment normally requires close cooperation with SAP for compliance with related standards.

Access to the full report requires a subscription to ISG Research. Please contact us for subscription inquiries.

Page Count: 34

QUESTIONS?

To purchase this product or for more information, please contact your account manager: