Play audio

Executive Summary

Customer Interaction Analytics

The first iteration of artificial intelligence (AI) tools for contact centers to use Generative AI (GenAI) brought measurable improvements to operations by automating routine functions and speeding interactions. What floated under the radar was how continued AI development was about to remake the analytic landscape around customers. We are now seeing the fruits of that process, as sophisticated analytics tools are hitting the market. These applications use real-time data about customers and interactions to help enterprises draw nuanced pictures of customers’ needs and intents, and allow businesses to measure the real-world impact of contact center operations on behavior, spending and loyalty.

Contact centers have remained largely unchanged for decades, but are now undergoing a drastic overhaul in operations, interaction mechanics and underlying technology architectures. This is proving disruptive to both technology buyers and sellers. The most immediate cause is the explosion of new tools derived from AI. Contact centers have always operated as reactive, cost-sensitive entities purpose-built for a narrowly defined function. Now centers are being asked to expand core functions, re-task the human labor force, respond to customers and enterprises in real time and use data for more sophisticated decision-making. In a short period, the foundational assumptions related to outfitting contact centers have been upended.

ISG Research defines the Customer Interaction Analytics category as tools built to provide insights into customer relationships.

ISG Research defines the Customer Interaction Analytics category as tools built to provide insights into customer relationships, using data specifically gathered from interactions and combined with other enterprise resources to enhance interaction data. It has many of the same elements as standard enterprise analytics, but is distinguished by its focus on interpreting customer intent and the performance of customer-based systems. It can also be viewed as an extension of prior generations of contact center reporting tools focused on maximizing productivity to control costs, but with added capabilities to analyze broader stretches of the customer lifecycle. Marketers use Customer Interaction Analytics to understand behavioral intent and purchasing patterns in much the same way as it is used to assess the efficiency of call handling.

Contact centers were first developed as business entities almost 50 years ago, and for much of that time, core technology and operations remained fairly stable. Well into the digital era, the fundamentals of interaction routing and workforce optimization were standard practices, augmented but not displaced by incremental innovations in expanding the channel landscape, more powerful analysis and better ways to measure performance.

The past three years have seen more disruptive innovation than centers have experienced to date. Much is made of the importance of AI in creating entirely new tools, and indeed, we assert that by 2027, three-quarters of contact centers will have introduced multiple GenAI applications into their service processes for routing, chatbots and agent assistance . But less discussion surrounds the impact of outside providers entering the contact center software space from adjacent markets, especially the hyperscaler giants. When firms with R&D resources in the tens of billions of dollars enter a market, the incumbent players have little choice but to make peace with a changed environment and adapt. The result has been an expansion of choice. In the past, a buyer had to select the core call-routing engine and build a center’s tech stack around that software provider’s solution. In the new world, hyperscalers have commoditized the routing engine, allowing virtually anyone—buyer or another provider—to build a contact center infrastructure based on whichever software component is most important to them. So, a buyer committed to a particular CRM or case-tracking tool can start with those elements and build the center using the extensive integrations and partnership networks available. Or, they can work with software from the back office or marketing department and conform the center’s systems to accommodate those applications.

. But less discussion surrounds the impact of outside providers entering the contact center software space from adjacent markets, especially the hyperscaler giants. When firms with R&D resources in the tens of billions of dollars enter a market, the incumbent players have little choice but to make peace with a changed environment and adapt. The result has been an expansion of choice. In the past, a buyer had to select the core call-routing engine and build a center’s tech stack around that software provider’s solution. In the new world, hyperscalers have commoditized the routing engine, allowing virtually anyone—buyer or another provider—to build a contact center infrastructure based on whichever software component is most important to them. So, a buyer committed to a particular CRM or case-tracking tool can start with those elements and build the center using the extensive integrations and partnership networks available. Or, they can work with software from the back office or marketing department and conform the center’s systems to accommodate those applications.

This means that providers from many origin points can plausibly go to market with a software suite that serves the core needs of contact centers—routing and workforce management. Buyers then distinguish between options based on more broad-based needs, such as data management, back-office integration, conformity with existing legacy tools or something specific to the unique business or vertical market. In 2025, contact center buyers face more—and more complicated—choices than ever.

What enterprises need is assurance of interoperability and clean, easy integrations. Most buyers appear to source technology from as few providers as possible, leaning toward suites for simplicity of administration. Most large and midsized platform providers encourage this by forging extensive partnership networks and app marketplaces that let buyers fill peripheral software needs with best-of-breed niche tools, with the assurance that the platform provider will coordinate the connections.

Enterprises that have not purchased contact center systems since before the pandemic (which is most of them) are experiencing a different world: new providers, providers that have evolved focus and a set of functional capabilities that didn’t exist five years ago. Business requirements have not advanced as quickly as technological innovation, so buyers are understandably reticent—even confused—about how to prioritize deployment of a new system. It doesn’t help that many contact center buyers are now also sitting side-by-side with CX professionals who have different, parallel goals for software purchases, and are simultaneously under great pressure from executives to stay current on developing AI technologies (if that is even possible).

All of that said, what enterprises really need to do is focus on two things: the foundational elements of yore, meaning routing and workforce tools, and the expanded universe of tools that support and extend its mission. Those would include advanced analytics, conversational AI for self-service, AI tools for automating quality and knowledge resources that feed the customer-facing AI.

Buyers also need assurance that when they take the leap into the realm of the new, they have concrete ROI metrics to back them up. Providers report a consistently high portion of AI-related sales riding atop detailed proof-of-concept trials. Some also indicate that the uptake for certain AI tools is correspondingly slow, as buyers wait for the proof points.

To meet these enterprise needs, today’s contact center systems must incorporate key AI applications that make up the current “core” capabilities: information synthesis and delivery to customers and human agents, automating processes within the center and between departments and analyzing customer sentiment more deeply than just at the level of the interaction. Contemporary tools need to be strong in areas that were once peripheral, especially self-service and analytics.

Of all the software areas related to contact center operations, agent management, customer analytics and self-service are the most dynamic, and most affected by AI innovation. Advanced analytics is particularly important in helping knit together contact centers with other teams into true enterprise CX projects. These efforts have been hampered by siloed processes and isolated data and systems. Customer interaction analytics can function as a bridge between the cost-sensitive workers who operate contact centers and revenue- and growth-focused workers in other CX roles.

The ISG Buyers Guide™ for Customer Interaction Analytics evaluates software providers and products in key areas, including omnichannel interaction capture, speech and text analytics, sentiment and behavioral analysis, intent recognition, predictive analytics, real-time dashboards and reporting, agent performance analysis and broad integrations to other applications.

This research evaluates the following software providers offering products to address key elements of Customer Interaction Analytics as we define it: 8x8, Aircall, Alvaria, Avaya, AWS, Calabrio, CallMiner, Cisco, Content Guru, Dialpad, Emplifi, Enghouse Interactive, Exotel, Five9, Genesys, GoTo, Microsoft, Mitel, net2phone, Nextiva, NiCE, Odigo, RingCentral, Salesforce, Sinch, Sprinklr, Talkdesk, Twilio, UJET, Verint, Vonage, XTIUM, Zendesk, Zoho and Zoom.

Buyers Guide Overview

For over two decades, ISG Research has conducted market research in a spectrum of areas across business applications, tools and technologies. We have designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of the business requirements in any enterprise. Utilization of our research methodology and decades of experience enables our Buyers Guide to be an effective method to assess and select software providers and products. The findings of this research undertaking contribute to our comprehensive approach to rating software providers in a manner that is based on the assessments completed by an enterprise.

ISG Research has designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of business requirements in any enterprise.

The ISG Buyers Guide™ for Customer Interaction Analytics is the distillation of over a year of market and product research efforts. It is an assessment of how well software providers’ offerings address enterprises’ requirements for customer interaction analytics software. The index is structured to support a request for information (RFI) that could be used in the request for proposal (RFP) process by incorporating all criteria needed to evaluate, select, utilize and maintain relationships with software providers. An effective product and customer experience with a provider can ensure the best long-term relationship and value achieved from a resource and financial investment.

In this Buyers Guide, ISG Research evaluates the software in seven key categories that are weighted to reflect buyers’ needs based on our expertise and research. Five are product-experience related: Adaptability, Capability, Manageability, Reliability, and Usability. In addition, we consider two customer-experience categories: Validation, and Total Cost of Ownership/Return on Investment (TCO/ROI). To assess functionality, one of the components of Capability, we applied the ISG Research Value Index methodology and blueprint, which links the personas and processes for customer interaction analytics to an enterprise’s requirements.

The structure of the research reflects our understanding that the effective evaluation of software providers and products involves far more than just examining product features, potential revenue or customers generated from a provider’s marketing and sales efforts. We believe it is important to take a comprehensive, research-based approach, since making the wrong choice of customer interaction analytics technology can raise the total cost of ownership, lower the return on investment and hamper an enterprise’s ability to reach its full performance potential. In addition, this approach can reduce the project’s development and deployment time and eliminate the risk of relying on a short list of software providers that does not represent a best fit for your enterprise.

ISG Research believes that an objective review of software providers and products is a critical business strategy for the adoption and implementation of customer interaction analytics software and applications. An enterprise’s review should include a thorough analysis of both what is possible and what is relevant. We urge enterprises to do a thorough job of evaluating customer interaction analytics systems and tools and offer this Buyers Guide as both the results of our in-depth analysis of these providers and as an evaluation methodology.

Key Takeaways

Contact centers are optimizing the support of customer interaction analytics that evolves from simple reporting and dashboards. New tools now use real-time interaction data to interpret customer needs, predict behaviors and measure the impact of CX operations on loyalty and spend, and use AI. As a result, successful platforms must provide both foundational routing and workforce tools and expanded AI-powered analytics to better support and self-service and broader enterprise CX strategies.

Software Provider Summary

The research identifies NiCE, Verint and Genesys as the market leaders, with strengths across multiple categories, while providers such as Content Guru, Calabrio and Sprinklr demonstrated targeted capabilities. Classification placed NiCE, Verint and Genesys in the Exemplary quadrant alongside providers including Salesforce, RingCentral, Talkdesk, Twilio, Zendesk and Zoho. Providers such as AWS, Cisco, Microsoft, Avaya and Vonage were categorized as Innovative, Zoom as Assurance, and vendors such as 8x8, Mitel, Sinch and Nextiva in the Merit quadrant. This segmentation enables enterprises to quickly assess which providers deliver the strongest overall balance of product and customer experience.

Product Experience Insights

Product Experience accounted for 80% of the overall rating, with emphasis on capability, usability, reliability, adaptability and manageability. NiCE, Verint and Genesys led in delivering advanced interaction analytics, workforce and quality management tools, while Five9 and Calabrio demonstrated strong but narrower capabilities. Leaders distinguished themselves with adaptability, usability and reliability, ensuring that their platforms can scale across enterprise requirements while supporting the adoption of AI-driven innovations.

Customer Experience Value

Customer Experience represented 20% of the evaluation, focused on validation and TCO/ROI. Verint, NiCE and Content Guru led in this category by demonstrating strong customer commitment, clear ROI frameworks, and lifecycle support. Genesys, Salesforce and Calabrio also performed well, though just short of leadership. Providers that ranked lower often lacked clarity in their CX, making it more difficult for enterprises to justify long-term investments.

Strategic Recommendations

Enterprises should view customer interaction analytics as a strategic investment that connects core contact center functions with advanced AI-driven insights into behavior, intent and sentiment. Buyers should prioritize platforms that integrate seamlessly with existing CX systems, deliver actionable analytics across the customer lifecycle and provide measurable ROI through proof-of-concepts. Using the ISG Buyers Guide helps enterprises assess and select solutions that improve efficiency and enhance overall experience.

How To Use This Buyers Guide

Evaluating Software Providers: The Process

We recommend using the Buyers Guide to assess and evaluate new or existing software providers for your enterprise. The market research can be used as an evaluation framework to establish a formal request for information from providers on products and customer experience and will shorten the cycle time when creating an RFI. The steps listed below provide a process that can facilitate best possible outcomes.

- Define the business case and goals.

Define the mission and business case for investment and the expected outcomes from your organizational and technology efforts. - Specify the business needs.

Defining the business requirements helps identify what specific capabilities are required with respect to people, processes, information and technology. - Assess the required roles and responsibilities. Identify the individuals required for success at every level of the organization from executives to front line workers and determine the needs of each.

- Outline the project’s critical path. What needs to be done, in what order and who will do it? This outline should make clear the prior dependencies at each step of the project plan.

- Ascertain the technology approach. Determine the business and technology approach that most closely aligns to your organization’s requirements.

- Establish technology vendor evaluation criteria. Utilize the product experience: Adaptability, Capability, Manageability, Reliability and Usability, and the customer experience in TCO/ROI and Validation.

- Evaluate and select the technology properly. Weight the categories in the technology evaluation criteria to reflect your organization’s priorities to determine the short list of vendors and products.

- Establish the business initiative team to start the project. Identify who will lead the project and the members of the team needed to plan and execute it with timelines, priorities and resources.

The Findings

All of the products we evaluated are feature-rich, but not all the capabilities offered by a software provider are equally valuable to types of workers or support everything needed to manage products on a continuous basis. Moreover, the existence of too many capabilities may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a larger number of features in the product is a plus, especially if some of them match your enterprise’s established practices or support an initiative that is driving the purchase of new software.

Factors beyond features and functions or software provider assessments may become a deciding factor. For example, an enterprise may face budget constraints such that the TCO evaluation can tip the balance to one provider or another. This is where the Value Index methodology and the appropriate category weighting can be applied to determine the best fit of software providers and products to your specific needs.

Overall Scoring of Software Providers Across Categories

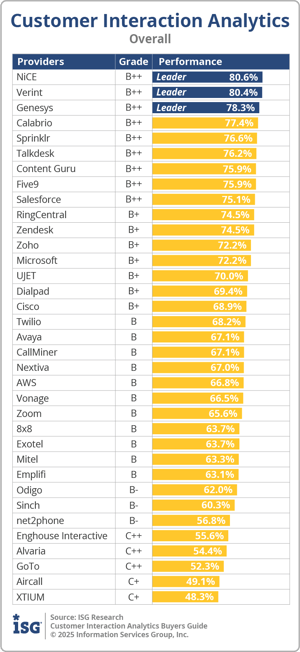

The research finds NiCE atop the list, followed by Verint and Genesys. Providers that place in the top three of a category earn the designation of Leader. NiCE has done so in seven categories; Verint in six; Genesys in three; Content Guru in two; and Calabrio, Sprinklr and Talkdesk in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have a higher weighted performance to the axis in aggregate of the five product categories place farther to the right, while the performance and weighting for the two Customer Experience categories determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research places software providers into one of four overall categories: Assurance, Exemplary, Merit or Innovative. This representation classifies providers’ overall weighted performance.

Exemplary: The categorization and placement of software providers in Exemplary (upper right) represent those that performed the best in meeting the overall Product and Customer Experience requirements. The providers rated Exemplary are: Calabrio, Content Guru, Dialpad, Five9, Genesys, NiCE, RingCentral, Salesforce, Sprinklr, Talkdesk, Twilio, Verint, Zendesk and Zoho.

Innovative: The categorization and placement of software providers in Innovative (lower right) represent those that performed the best in meeting the overall Product Experience requirements but did not achieve the highest levels of requirements in Customer Experience. The providers rated Innovative are: Avaya, AWS, CallMiner, Cisco, Microsoft, Nextiva, UJET and Vonage.

Assurance: The categorization and placement of software providers in Assurance (upper left) represent those that achieved the highest levels in the overall Customer Experience requirements but did not achieve the highest levels of Product Experience. The provider rated Assurance is: Zoom.

Merit: The categorization of software providers in Merit (lower left) represents those that did not surpass the thresholds for the Assurance, Exemplary or Innovative categories in Customer or Product Experience. The providers rated Merit are: 8x8, Aircall, Alvaria, Emplifi, Enghouse Interactive, Exotel, GoTo, Mitel, net2phone, Odigo, Sinch and Xtium.

We warn that close provider placement proximity should not be taken to imply that the packages evaluated are functionally identical or equally well suited for use by every enterprise or for a specific process. Although there is a high degree of commonality in how enterprises handle customer interaction analytics, there are many idiosyncrasies and differences in how they do these functions that can make one software provider’s offering a better fit than another’s for a particular enterprise’s needs.

We advise enterprises to assess and evaluate software providers based on organizational requirements and use this research as a supplement to internal evaluation of a provider and products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive. Our Value Index methodology examines Product Experience and how it aligns with an enterprise’s lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future, which are flawed since they do not represent an enterprise’s requirements but how the provider operates. As more software providers orient to a complete product experience, evaluations will be more robust.

comprehensive. Our Value Index methodology examines Product Experience and how it aligns with an enterprise’s lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future, which are flawed since they do not represent an enterprise’s requirements but how the provider operates. As more software providers orient to a complete product experience, evaluations will be more robust.

The research results in Product Experience are ranked at 80%, or four-fifths, of the overall rating using the specific underlying weighted category performance. Importance was placed on the categories as follows: Usability (10%), Capability (40%), Reliability (10%), Adaptability (10%) and Manageability (10%). This weighting impacted the resulting overall ratings in this research. NiCE, Verint and Genesys were designated Product Experience Leaders. While not a Leader, Calabrio was also found to meet a broad range of enterprise product experience requirements.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The advancement of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. Technology providers that have chief customer officers are more likely to have greater investments in the customer relationship and focus more on their success. These leaders also need to take responsibility for ensuring this commitment is made abundantly clear on the website and in the buying process and customer journey.

customer officers are more likely to have greater investments in the customer relationship and focus more on their success. These leaders also need to take responsibility for ensuring this commitment is made abundantly clear on the website and in the buying process and customer journey.

The research results in Customer Experience are ranked at 20%, or one-fifth, using the specific underlying weighted category performance as it relates to the framework of commitment and value to the software provider-customer relationship. The two evaluation categories are Validation (10%) and TCO/ROI (10%), which are weighted to represent their importance to the overall research.

The software providers that evaluated the highest overall in the aggregated and weighted Customer Experience categories are Verint, NiCE and Content Guru. These category Leaders best communicate commitment and dedication to customer needs. While not Leaders, Genesys, Salesforce and Calabrio were also found to meet a broad range of enterprise customer experience requirements.

Software providers that did not perform well in this category were unable to provide sufficient customer case studies to demonstrate success or articulate their commitment to customer experience and an enterprise’s journey. The selection of a software provider means a continuous investment by the enterprise, so a holistic evaluation must include examination of how they support their customer experience.

Appendix: Software Provider Inclusion

For inclusion in the ISG Buyers Guide™ for Customer Interaction Analytics in 2025, a software provider must have a standalone software application (or suite of applications) that serves the operating needs of contact centers, including routing, workforce engagement, analysis and customer data management.

The firm must be in good standing financially and ethically, have at least $50 million in annual or projected revenue, more than 50 employees, sell products and provide support on at least two continents, and have at least 25 customers. The principal source of the relevant business unit’s revenue must be software-related and there must have been at least one major software release in the last 12 months. To qualify for evaluation in Customer Interaction Analytics, the product should include most of the following capabilities: omnichannel interaction capture; speech and text analytics; sentiment and behavioral analysis; intent recognition; predictive analytics; real-time dashboards and reporting; agent performance analysis; and broad integrations to other applications.

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer suites or packages of products that may include relevant individual modules or applications. If a software provider is actively marketing, selling and developing a product for the general market and it is reflected on the provider’s website that the product is within the scope of the research, that provider is automatically evaluated for inclusion.

All software providers that offer relevant customer interaction analytics products and meet the inclusion requirements were invited to participate in the evaluation process at no cost to them.

Software providers that meet our inclusion criteria but did not completely participate in our Buyers Guide were assessed solely on publicly available information. As this could have a significant impact on classification and ratings, we recommend additional scrutiny when evaluating those providers.

Products Evaluated

|

Provider |

Product Names |

Version |

Release |

|

8x8 |

8x8 Contact Center |

9.16 |

April 2025 |

|

Aircall |

Aircall Workspace, Aircall Conversation Center |

June 2025 |

June 2025 |

|

Alvaria |

Alvaria CXP, Alvaria Intelligence Platform, Alvaria Cloud |

CXP v. 24 |

May 2025 |

|

Avaya |

Avaya Infinity Platform; Avaya Experience Platform |

1.0.9 |

June 2025 |

|

AWS |

Amazon Connect |

May 2025 |

May 2025 |

|

Calabrio |

Calabrio ONE |

2508.3.1 |

June 2025 |

|

CallMiner |

CallMiner Eureka Platform |

2025.06 |

June 2025 |

|

Cisco |

Webex Contact Center |

June 2025 |

June 2025 |

|

Content Guru |

storm CONTACT |

June 2025 |

June 2025 |

|

Dialpad |

Dialpad Support |

25.06.03 |

June 2025 |

|

Emplifi |

Emplifi Platform |

June 2025 |

June 2025 |

|

Enghouse Interactive |

Enghouse Contact Center Enterprise |

24.3 |

March 2024 |

|

Exotel |

Exotel Enterprise Contact Center |

June 2025 |

June 2025 |

|

Five9 |

Five9 Intelligent Cloud Contact Center Platform |

June 2025 |

June 2025 |

|

Genesys |

Genesys Cloud CX, Genesys Cloud EX |

June 2025 |

June 2025 |

|

GoTo |

GoTo Connect Contact Center |

May 2025 |

May 2025 |

|

Microsoft |

Dynamics 365 Contact Center |

Release Wave 1 |

April 2025 |

|

Mitel |

Mitel CX |

1.0 |

July 2025 |

|

net2phone |

uContact |

July 2025 |

July 2025 |

|

Nextiva |

Nextiva Unified Customer Experience Management Platform |

April 2025 |

April 2025 |

|

NiCE |

NiCE CXone Mpower |

June 2025 |

June 2025 |

|

Odigo |

Odigo Platform |

June 2025 |

June 2025 |

|

RingCentral |

RingCX, RingCentral Contact Center Enterprise |

25.2 |

April 2025 |

|

Salesforce |

Salesforce Service Cloud |

Summer '25 |

June 2025 |

|

Sinch |

Sinch Contact Pro |

7.0 FP17 (7.0.17.0) Release |

June 2025 |

|

Sprinklr |

Sprinklr Service |

20.4 |

June 2025 |

|

Talkdesk |

Talkdesk CX Cloud |

April 2025 |

April 2025 |

|

Twilio |

Twilio Customer Engagement Platform |

Q1 2025 |

June 2025 |

|

UJET |

UJET Platform |

June 2025 |

June 2025 |

|

Verint |

Verint |

2025R1 |

May 2025 |

|

Vonage |

Vonage Fusion, Vonage Contact Center |

2025.1 |

February 2025 |

|

XTIUM |

XTIUM Contact Suite |

2025.7 |

July 2025 |

|

Zendesk |

Zendesk Resolution Platform, Zendesk for Contact Center |

June 2025 |

June 2025 |

|

Zoho |

Zoho Voice, Zoho Service Plus |

Spring 2025 |

June 2025 |

|

Zoom |

Zoom Contact Center |

June 2025 |

June 2025 |

Providers of Promise

We did not include software providers that, as a result of our research and analysis, did not satisfy the criteria for inclusion in this Buyers Guide. These are listed below as “Providers of Promise.”

|

Provider |

Product |

Capabilities |

Revenue |

Geography |

Customers |

|

Aloware |

Contact Center Software |

Yes |

No |

Yes |

Yes |

|

AnywhereNow |

Dialogue Cloud Neo |

No |

Yes |

Yes |

Yes |

|

ASC Technologies |

Neo Suite; Recording Insights |

No |

No |

Yes |

Yes |

|

Avoxi |

AVOXI Contact Center |

No |

Yes |

Yes |

Yes |

|

Call Center Studio |

Contact Center Management Software |

Yes |

No |

Yes |

Yes |

|

CallTools |

Power Contact Center |

No |

No |

No |

No |

|

CloudTalk |

CloudTalk Inbound Call Center |

No |

No |

Yes |

Yes |

|

ComputerTalk |

ice Contact Center |

Yes |

No |

Yes |

Yes |

|

Dixa |

Conversational Customer Service Platform |

Yes |

No |

Yes |

Yes |

|

Gladly |

Gladly Platform, Gladly Sidekick |

No |

No |

Yes |

Yes |

|

Puzzel |

Puzzel Contact Centre |

Yes |

No |

No |

Yes |

|

Sharpen |

Sharpen CCaaS Platform |

Yes |

No |

Yes |

Yes |

|

Vocalcom |

Vocalcom Hermes360 |

No |

Yes |

Yes |

Yes |

|

Xima |

Contact Center Cloud |

Yes |

No |

Yes |

Yes |

Executive Summary

Customer Interaction Analytics

The first iteration of artificial intelligence (AI) tools for contact centers to use Generative AI (GenAI) brought measurable improvements to operations by automating routine functions and speeding interactions. What floated under the radar was how continued AI development was about to remake the analytic landscape around customers. We are now seeing the fruits of that process, as sophisticated analytics tools are hitting the market. These applications use real-time data about customers and interactions to help enterprises draw nuanced pictures of customers’ needs and intents, and allow businesses to measure the real-world impact of contact center operations on behavior, spending and loyalty.

Contact centers have remained largely unchanged for decades, but are now undergoing a drastic overhaul in operations, interaction mechanics and underlying technology architectures. This is proving disruptive to both technology buyers and sellers. The most immediate cause is the explosion of new tools derived from AI. Contact centers have always operated as reactive, cost-sensitive entities purpose-built for a narrowly defined function. Now centers are being asked to expand core functions, re-task the human labor force, respond to customers and enterprises in real time and use data for more sophisticated decision-making. In a short period, the foundational assumptions related to outfitting contact centers have been upended.

ISG Research defines the Customer Interaction Analytics category as tools built to provide insights into customer relationships.

ISG Research defines the Customer Interaction Analytics category as tools built to provide insights into customer relationships, using data specifically gathered from interactions and combined with other enterprise resources to enhance interaction data. It has many of the same elements as standard enterprise analytics, but is distinguished by its focus on interpreting customer intent and the performance of customer-based systems. It can also be viewed as an extension of prior generations of contact center reporting tools focused on maximizing productivity to control costs, but with added capabilities to analyze broader stretches of the customer lifecycle. Marketers use Customer Interaction Analytics to understand behavioral intent and purchasing patterns in much the same way as it is used to assess the efficiency of call handling.

Contact centers were first developed as business entities almost 50 years ago, and for much of that time, core technology and operations remained fairly stable. Well into the digital era, the fundamentals of interaction routing and workforce optimization were standard practices, augmented but not displaced by incremental innovations in expanding the channel landscape, more powerful analysis and better ways to measure performance.

The past three years have seen more disruptive innovation than centers have experienced to date. Much is made of the importance of AI in creating entirely new tools, and indeed, we assert that by 2027, three-quarters of contact centers will have introduced multiple GenAI applications into their service processes for routing, chatbots and agent assistance. But less discussion surrounds the impact of outside providers entering the contact center software space from adjacent markets, especially the hyperscaler giants. When firms with R&D resources in the tens of billions of dollars enter a market, the incumbent players have little choice but to make peace with a changed environment and adapt. The result has been an expansion of choice. In the past, a buyer had to select the core call-routing engine and build a center’s tech stack around that software provider’s solution. In the new world, hyperscalers have commoditized the routing engine, allowing virtually anyone—buyer or another provider—to build a contact center infrastructure based on whichever software component is most important to them. So, a buyer committed to a particular CRM or case-tracking tool can start with those elements and build the center using the extensive integrations and partnership networks available. Or, they can work with software from the back office or marketing department and conform the center’s systems to accommodate those applications.

This means that providers from many origin points can plausibly go to market with a software suite that serves the core needs of contact centers—routing and workforce management. Buyers then distinguish between options based on more broad-based needs, such as data management, back-office integration, conformity with existing legacy tools or something specific to the unique business or vertical market. In 2025, contact center buyers face more—and more complicated—choices than ever.

What enterprises need is assurance of interoperability and clean, easy integrations. Most buyers appear to source technology from as few providers as possible, leaning toward suites for simplicity of administration. Most large and midsized platform providers encourage this by forging extensive partnership networks and app marketplaces that let buyers fill peripheral software needs with best-of-breed niche tools, with the assurance that the platform provider will coordinate the connections.

Enterprises that have not purchased contact center systems since before the pandemic (which is most of them) are experiencing a different world: new providers, providers that have evolved focus and a set of functional capabilities that didn’t exist five years ago. Business requirements have not advanced as quickly as technological innovation, so buyers are understandably reticent—even confused—about how to prioritize deployment of a new system. It doesn’t help that many contact center buyers are now also sitting side-by-side with CX professionals who have different, parallel goals for software purchases, and are simultaneously under great pressure from executives to stay current on developing AI technologies (if that is even possible).

All of that said, what enterprises really need to do is focus on two things: the foundational elements of yore, meaning routing and workforce tools, and the expanded universe of tools that support and extend its mission. Those would include advanced analytics, conversational AI for self-service, AI tools for automating quality and knowledge resources that feed the customer-facing AI.

Buyers also need assurance that when they take the leap into the realm of the new, they have concrete ROI metrics to back them up. Providers report a consistently high portion of AI-related sales riding atop detailed proof-of-concept trials. Some also indicate that the uptake for certain AI tools is correspondingly slow, as buyers wait for the proof points.

To meet these enterprise needs, today’s contact center systems must incorporate key AI applications that make up the current “core” capabilities: information synthesis and delivery to customers and human agents, automating processes within the center and between departments and analyzing customer sentiment more deeply than just at the level of the interaction. Contemporary tools need to be strong in areas that were once peripheral, especially self-service and analytics.

Of all the software areas related to contact center operations, agent management, customer analytics and self-service are the most dynamic, and most affected by AI innovation. Advanced analytics is particularly important in helping knit together contact centers with other teams into true enterprise CX projects. These efforts have been hampered by siloed processes and isolated data and systems. Customer interaction analytics can function as a bridge between the cost-sensitive workers who operate contact centers and revenue- and growth-focused workers in other CX roles.

The ISG Buyers Guide™ for Customer Interaction Analytics evaluates software providers and products in key areas, including omnichannel interaction capture, speech and text analytics, sentiment and behavioral analysis, intent recognition, predictive analytics, real-time dashboards and reporting, agent performance analysis and broad integrations to other applications.

This research evaluates the following software providers offering products to address key elements of Customer Interaction Analytics as we define it: 8x8, Aircall, Alvaria, Avaya, AWS, Calabrio, CallMiner, Cisco, Content Guru, Dialpad, Emplifi, Enghouse Interactive, Exotel, Five9, Genesys, GoTo, Microsoft, Mitel, net2phone, Nextiva, NiCE, Odigo, RingCentral, Salesforce, Sinch, Sprinklr, Talkdesk, Twilio, UJET, Verint, Vonage, XTIUM, Zendesk, Zoho and Zoom.

Buyers Guide Overview

For over two decades, ISG Research has conducted market research in a spectrum of areas across business applications, tools and technologies. We have designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of the business requirements in any enterprise. Utilization of our research methodology and decades of experience enables our Buyers Guide to be an effective method to assess and select software providers and products. The findings of this research undertaking contribute to our comprehensive approach to rating software providers in a manner that is based on the assessments completed by an enterprise.

ISG Research has designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of business requirements in any enterprise.

The ISG Buyers Guide™ for Customer Interaction Analytics is the distillation of over a year of market and product research efforts. It is an assessment of how well software providers’ offerings address enterprises’ requirements for customer interaction analytics software. The index is structured to support a request for information (RFI) that could be used in the request for proposal (RFP) process by incorporating all criteria needed to evaluate, select, utilize and maintain relationships with software providers. An effective product and customer experience with a provider can ensure the best long-term relationship and value achieved from a resource and financial investment.

In this Buyers Guide, ISG Research evaluates the software in seven key categories that are weighted to reflect buyers’ needs based on our expertise and research. Five are product-experience related: Adaptability, Capability, Manageability, Reliability, and Usability. In addition, we consider two customer-experience categories: Validation, and Total Cost of Ownership/Return on Investment (TCO/ROI). To assess functionality, one of the components of Capability, we applied the ISG Research Value Index methodology and blueprint, which links the personas and processes for customer interaction analytics to an enterprise’s requirements.

The structure of the research reflects our understanding that the effective evaluation of software providers and products involves far more than just examining product features, potential revenue or customers generated from a provider’s marketing and sales efforts. We believe it is important to take a comprehensive, research-based approach, since making the wrong choice of customer interaction analytics technology can raise the total cost of ownership, lower the return on investment and hamper an enterprise’s ability to reach its full performance potential. In addition, this approach can reduce the project’s development and deployment time and eliminate the risk of relying on a short list of software providers that does not represent a best fit for your enterprise.

ISG Research believes that an objective review of software providers and products is a critical business strategy for the adoption and implementation of customer interaction analytics software and applications. An enterprise’s review should include a thorough analysis of both what is possible and what is relevant. We urge enterprises to do a thorough job of evaluating customer interaction analytics systems and tools and offer this Buyers Guide as both the results of our in-depth analysis of these providers and as an evaluation methodology.

Key Takeaways

Contact centers are optimizing the support of customer interaction analytics that evolves from simple reporting and dashboards. New tools now use real-time interaction data to interpret customer needs, predict behaviors and measure the impact of CX operations on loyalty and spend, and use AI. As a result, successful platforms must provide both foundational routing and workforce tools and expanded AI-powered analytics to better support and self-service and broader enterprise CX strategies.

Software Provider Summary

The research identifies NiCE, Verint and Genesys as the market leaders, with strengths across multiple categories, while providers such as Content Guru, Calabrio and Sprinklr demonstrated targeted capabilities. Classification placed NiCE, Verint and Genesys in the Exemplary quadrant alongside providers including Salesforce, RingCentral, Talkdesk, Twilio, Zendesk and Zoho. Providers such as AWS, Cisco, Microsoft, Avaya and Vonage were categorized as Innovative, Zoom as Assurance, and vendors such as 8x8, Mitel, Sinch and Nextiva in the Merit quadrant. This segmentation enables enterprises to quickly assess which providers deliver the strongest overall balance of product and customer experience.

Product Experience Insights

Product Experience accounted for 80% of the overall rating, with emphasis on capability, usability, reliability, adaptability and manageability. NiCE, Verint and Genesys led in delivering advanced interaction analytics, workforce and quality management tools, while Five9 and Calabrio demonstrated strong but narrower capabilities. Leaders distinguished themselves with adaptability, usability and reliability, ensuring that their platforms can scale across enterprise requirements while supporting the adoption of AI-driven innovations.

Customer Experience Value

Customer Experience represented 20% of the evaluation, focused on validation and TCO/ROI. Verint, NiCE and Content Guru led in this category by demonstrating strong customer commitment, clear ROI frameworks, and lifecycle support. Genesys, Salesforce and Calabrio also performed well, though just short of leadership. Providers that ranked lower often lacked clarity in their CX, making it more difficult for enterprises to justify long-term investments.

Strategic Recommendations

Enterprises should view customer interaction analytics as a strategic investment that connects core contact center functions with advanced AI-driven insights into behavior, intent and sentiment. Buyers should prioritize platforms that integrate seamlessly with existing CX systems, deliver actionable analytics across the customer lifecycle and provide measurable ROI through proof-of-concepts. Using the ISG Buyers Guide helps enterprises assess and select solutions that improve efficiency and enhance overall experience.

How To Use This Buyers Guide

Evaluating Software Providers: The Process

We recommend using the Buyers Guide to assess and evaluate new or existing software providers for your enterprise. The market research can be used as an evaluation framework to establish a formal request for information from providers on products and customer experience and will shorten the cycle time when creating an RFI. The steps listed below provide a process that can facilitate best possible outcomes.

- Define the business case and goals.

Define the mission and business case for investment and the expected outcomes from your organizational and technology efforts. - Specify the business needs.

Defining the business requirements helps identify what specific capabilities are required with respect to people, processes, information and technology. - Assess the required roles and responsibilities. Identify the individuals required for success at every level of the organization from executives to front line workers and determine the needs of each.

- Outline the project’s critical path. What needs to be done, in what order and who will do it? This outline should make clear the prior dependencies at each step of the project plan.

- Ascertain the technology approach. Determine the business and technology approach that most closely aligns to your organization’s requirements.

- Establish technology vendor evaluation criteria. Utilize the product experience: Adaptability, Capability, Manageability, Reliability and Usability, and the customer experience in TCO/ROI and Validation.

- Evaluate and select the technology properly. Weight the categories in the technology evaluation criteria to reflect your organization’s priorities to determine the short list of vendors and products.

- Establish the business initiative team to start the project. Identify who will lead the project and the members of the team needed to plan and execute it with timelines, priorities and resources.

The Findings

All of the products we evaluated are feature-rich, but not all the capabilities offered by a software provider are equally valuable to types of workers or support everything needed to manage products on a continuous basis. Moreover, the existence of too many capabilities may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a larger number of features in the product is a plus, especially if some of them match your enterprise’s established practices or support an initiative that is driving the purchase of new software.

Factors beyond features and functions or software provider assessments may become a deciding factor. For example, an enterprise may face budget constraints such that the TCO evaluation can tip the balance to one provider or another. This is where the Value Index methodology and the appropriate category weighting can be applied to determine the best fit of software providers and products to your specific needs.

Overall Scoring of Software Providers Across Categories

The research finds NiCE atop the list, followed by Verint and Genesys. Providers that place in the top three of a category earn the designation of Leader. NiCE has done so in seven categories; Verint in six; Genesys in three; Content Guru in two; and Calabrio, Sprinklr and Talkdesk in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have a higher weighted performance to the axis in aggregate of the five product categories place farther to the right, while the performance and weighting for the two Customer Experience categories determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research places software providers into one of four overall categories: Assurance, Exemplary, Merit or Innovative. This representation classifies providers’ overall weighted performance.

Exemplary: The categorization and placement of software providers in Exemplary (upper right) represent those that performed the best in meeting the overall Product and Customer Experience requirements. The providers rated Exemplary are: Calabrio, Content Guru, Dialpad, Five9, Genesys, NiCE, RingCentral, Salesforce, Sprinklr, Talkdesk, Twilio, Verint, Zendesk and Zoho.

Innovative: The categorization and placement of software providers in Innovative (lower right) represent those that performed the best in meeting the overall Product Experience requirements but did not achieve the highest levels of requirements in Customer Experience. The providers rated Innovative are: Avaya, AWS, CallMiner, Cisco, Microsoft, Nextiva, UJET and Vonage.

Assurance: The categorization and placement of software providers in Assurance (upper left) represent those that achieved the highest levels in the overall Customer Experience requirements but did not achieve the highest levels of Product Experience. The provider rated Assurance is: Zoom.

Merit: The categorization of software providers in Merit (lower left) represents those that did not surpass the thresholds for the Assurance, Exemplary or Innovative categories in Customer or Product Experience. The providers rated Merit are: 8x8, Aircall, Alvaria, Emplifi, Enghouse Interactive, Exotel, GoTo, Mitel, net2phone, Odigo, Sinch and Xtium.

We warn that close provider placement proximity should not be taken to imply that the packages evaluated are functionally identical or equally well suited for use by every enterprise or for a specific process. Although there is a high degree of commonality in how enterprises handle customer interaction analytics, there are many idiosyncrasies and differences in how they do these functions that can make one software provider’s offering a better fit than another’s for a particular enterprise’s needs.

We advise enterprises to assess and evaluate software providers based on organizational requirements and use this research as a supplement to internal evaluation of a provider and products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive. Our Value Index methodology examines Product Experience and how it aligns with an enterprise’s lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future, which are flawed since they do not represent an enterprise’s requirements but how the provider operates. As more software providers orient to a complete product experience, evaluations will be more robust.

The research results in Product Experience are ranked at 80%, or four-fifths, of the overall rating using the specific underlying weighted category performance. Importance was placed on the categories as follows: Usability (10%), Capability (40%), Reliability (10%), Adaptability (10%) and Manageability (10%). This weighting impacted the resulting overall ratings in this research. NiCE, Verint and Genesys were designated Product Experience Leaders. While not a Leader, Calabrio was also found to meet a broad range of enterprise product experience requirements.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The advancement of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. Technology providers that have chief customer officers are more likely to have greater investments in the customer relationship and focus more on their success. These leaders also need to take responsibility for ensuring this commitment is made abundantly clear on the website and in the buying process and customer journey.

The research results in Customer Experience are ranked at 20%, or one-fifth, using the specific underlying weighted category performance as it relates to the framework of commitment and value to the software provider-customer relationship. The two evaluation categories are Validation (10%) and TCO/ROI (10%), which are weighted to represent their importance to the overall research.

The software providers that evaluated the highest overall in the aggregated and weighted Customer Experience categories are Verint, NiCE and Content Guru. These category Leaders best communicate commitment and dedication to customer needs. While not Leaders, Genesys, Salesforce and Calabrio were also found to meet a broad range of enterprise customer experience requirements.

Software providers that did not perform well in this category were unable to provide sufficient customer case studies to demonstrate success or articulate their commitment to customer experience and an enterprise’s journey. The selection of a software provider means a continuous investment by the enterprise, so a holistic evaluation must include examination of how they support their customer experience.

Appendix: Software Provider Inclusion

For inclusion in the ISG Buyers Guide™ for Customer Interaction Analytics in 2025, a software provider must have a standalone software application (or suite of applications) that serves the operating needs of contact centers, including routing, workforce engagement, analysis and customer data management.

The firm must be in good standing financially and ethically, have at least $50 million in annual or projected revenue, more than 50 employees, sell products and provide support on at least two continents, and have at least 25 customers. The principal source of the relevant business unit’s revenue must be software-related and there must have been at least one major software release in the last 12 months. To qualify for evaluation in Customer Interaction Analytics, the product should include most of the following capabilities: omnichannel interaction capture; speech and text analytics; sentiment and behavioral analysis; intent recognition; predictive analytics; real-time dashboards and reporting; agent performance analysis; and broad integrations to other applications.

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer suites or packages of products that may include relevant individual modules or applications. If a software provider is actively marketing, selling and developing a product for the general market and it is reflected on the provider’s website that the product is within the scope of the research, that provider is automatically evaluated for inclusion.

All software providers that offer relevant customer interaction analytics products and meet the inclusion requirements were invited to participate in the evaluation process at no cost to them.

Software providers that meet our inclusion criteria but did not completely participate in our Buyers Guide were assessed solely on publicly available information. As this could have a significant impact on classification and ratings, we recommend additional scrutiny when evaluating those providers.

Products Evaluated

|

Provider |

Product Names |

Version |

Release |

|

8x8 |

8x8 Contact Center |

9.16 |

April 2025 |

|

Aircall |

Aircall Workspace, Aircall Conversation Center |

June 2025 |

June 2025 |

|

Alvaria |

Alvaria CXP, Alvaria Intelligence Platform, Alvaria Cloud |

CXP v. 24 |

May 2025 |

|

Avaya |

Avaya Infinity Platform; Avaya Experience Platform |

1.0.9 |

June 2025 |

|

AWS |

Amazon Connect |

May 2025 |

May 2025 |

|

Calabrio |

Calabrio ONE |

2508.3.1 |

June 2025 |

|

CallMiner |

CallMiner Eureka Platform |

2025.06 |

June 2025 |

|

Cisco |

Webex Contact Center |

June 2025 |

June 2025 |

|

Content Guru |

storm CONTACT |

June 2025 |

June 2025 |

|

Dialpad |

Dialpad Support |

25.06.03 |

June 2025 |

|

Emplifi |

Emplifi Platform |

June 2025 |

June 2025 |

|

Enghouse Interactive |

Enghouse Contact Center Enterprise |

24.3 |

March 2024 |

|

Exotel |

Exotel Enterprise Contact Center |

June 2025 |

June 2025 |

|

Five9 |

Five9 Intelligent Cloud Contact Center Platform |

June 2025 |

June 2025 |

|

Genesys |

Genesys Cloud CX, Genesys Cloud EX |

June 2025 |

June 2025 |

|

GoTo |

GoTo Connect Contact Center |

May 2025 |

May 2025 |

|

Microsoft |

Dynamics 365 Contact Center |

Release Wave 1 |

April 2025 |

|

Mitel |

Mitel CX |

1.0 |

July 2025 |

|

net2phone |

uContact |

July 2025 |

July 2025 |

|

Nextiva |

Nextiva Unified Customer Experience Management Platform |

April 2025 |

April 2025 |

|

NiCE |

NiCE CXone Mpower |

June 2025 |

June 2025 |

|

Odigo |

Odigo Platform |

June 2025 |

June 2025 |

|

RingCentral |

RingCX, RingCentral Contact Center Enterprise |

25.2 |

April 2025 |

|

Salesforce |

Salesforce Service Cloud |

Summer '25 |

June 2025 |

|

Sinch |

Sinch Contact Pro |

7.0 FP17 (7.0.17.0) Release |

June 2025 |

|

Sprinklr |

Sprinklr Service |

20.4 |

June 2025 |

|

Talkdesk |

Talkdesk CX Cloud |

April 2025 |

April 2025 |

|

Twilio |

Twilio Customer Engagement Platform |

Q1 2025 |

June 2025 |

|

UJET |

UJET Platform |

June 2025 |

June 2025 |

|

Verint |

Verint |

2025R1 |

May 2025 |

|

Vonage |

Vonage Fusion, Vonage Contact Center |

2025.1 |

February 2025 |

|

XTIUM |

XTIUM Contact Suite |

2025.7 |

July 2025 |

|

Zendesk |

Zendesk Resolution Platform, Zendesk for Contact Center |

June 2025 |

June 2025 |

|

Zoho |

Zoho Voice, Zoho Service Plus |

Spring 2025 |

June 2025 |

|

Zoom |

Zoom Contact Center |

June 2025 |

June 2025 |

Providers of Promise

We did not include software providers that, as a result of our research and analysis, did not satisfy the criteria for inclusion in this Buyers Guide. These are listed below as “Providers of Promise.”

|

Provider |

Product |

Capabilities |

Revenue |

Geography |

Customers |

|

Aloware |

Contact Center Software |

Yes |

No |

Yes |

Yes |

|

AnywhereNow |

Dialogue Cloud Neo |

No |

Yes |

Yes |

Yes |

|

ASC Technologies |

Neo Suite; Recording Insights |

No |

No |

Yes |

Yes |

|

Avoxi |

AVOXI Contact Center |

No |

Yes |

Yes |

Yes |

|

Call Center Studio |

Contact Center Management Software |

Yes |

No |

Yes |

Yes |

|

CallTools |

Power Contact Center |

No |

No |

No |

No |

|

CloudTalk |

CloudTalk Inbound Call Center |

No |

No |

Yes |

Yes |

|

ComputerTalk |

ice Contact Center |

Yes |

No |

Yes |

Yes |

|

Dixa |

Conversational Customer Service Platform |

Yes |

No |

Yes |

Yes |

|

Gladly |

Gladly Platform, Gladly Sidekick |

No |

No |

Yes |

Yes |

|

Puzzel |

Puzzel Contact Centre |

Yes |

No |

No |

Yes |

|

Sharpen |

Sharpen CCaaS Platform |

Yes |

No |

Yes |

Yes |

|

Vocalcom |

Vocalcom Hermes360 |

No |

Yes |

Yes |

Yes |

|

Xima |

Contact Center Cloud |

Yes |

No |

Yes |

Yes |

Fill out the form to continue reading.