Mark is the leader for software in AI advisory at ISG, responsible for AI-driven value streams and software blueprints that enable autonomous enterprises across industry, business, and IT. Prior to ISG, he founded Ventana Research, serving as CEO and Chief Research Officer, where he created the ISG Buyers Guides an enterprise decision-making framework delivering objective ratings and rankings across more than 200 software categories. A 35-year technology industry veteran, Mark has held senior leadership roles in product and marketing at SAP and Oracle, helping shape enterprise software strategy and market innovation. He is an Eagle Scout and an active Scouting volunteer, dedicated to helping young people reach their full potential.

narration area

Executive Summary

Buyers Guide Overview

ISG Research has conducted market research for over two decades across vertical industries, business applications, AI and IT. We have designed the ISG Buyers Guide™ to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements. Utilization of our research methodology and decades of experience enables our Buyers Guide to be an effective method to assess and select software providers and products. The findings of this research provide a comprehensive approach to rating software providers and rank their ability to meet specific product and customer experience requirements.

ISG Research has designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements.

The 2025 ISG Buyers Guides™ for Power and Utilities, covering Power and Utilities, Power and Utilities Digital Twin, Power and Utilities EAM, Power and Utilities Field Service and Power and Utilities Predictive Maintenance, are the distillation of continuous market and product research. It is an assessment of how well software providers’ offerings address enterprises’ requirements for power and utilities industry software. The Value Index methodology is structured to support a request for information (RFI) for a request for proposal (RFP) process by incorporating all criteria needed to evaluate, select, utilize and maintain relationships with software providers. The ISG Buyers Guide evaluates customer experience and the product experience in its capability and platform.

The structure of the research reflects our understanding that the effective evaluation of software providers and products involves far more than just examining product features, potential revenue or customers generated from a provider’s marketing and sales efforts. It can ensure the best long-term relationship and value achieved from a resource and financial investment We believe it is important to take a comprehensive, research-based approach, since making the wrong choice of software can raise the total cost of ownership, lower the return on investment and hamper an enterprise’s ability to reach its potential. In addition, this approach can reduce the project’s development and deployment time and eliminate the risk of relying on opinions or historical biases.

ISG Research believes that an objective review of existing and potential new software providers and products is a critical strategy for the adoption and implementation of power and utilities industry software. An enterprise’s review should include an analysis of both what is possible and what is relevant. We urge enterprises to do a thorough job of evaluating software and offer these Buyers Guides as both the results of our in-depth analysis of these providers and as an evaluation methodology.

How To Use This Buyers Guide

Evaluating Software Providers: The Process

We recommend using the Buyers Guide to assess and evaluate new or existing software providers for your enterprise. The market research can be used as an evaluation framework to assess existing approaches and software providers or establish a formal request for information from providers on products and customer experience and will shorten the cycle time when creating an RFI. The steps listed below provide a process that can facilitate best possible outcomes in the most efficient manner.

- Define the business case and goals.

Define the mission and business case for investment and the expected outcomes from your organizational and technological efforts.

- Specify the business and IT needs.

Defining the business and IT requirements helps identify what specific capabilities are required with respect to people, processes, information and technology.

- Assess the required roles and responsibilities.

Identify the individuals required for success at every level of the enterprise from executives to frontline workers and determine the needs of each.

- Outline the project’s critical path.

What needs to be done, in what order and who will do it? This outline should make clear the prior dependencies at each step of the project plan.

- Ascertain the technology approach.

Determine the business and technology approach that most closely aligns to your enterprise’s requirements.

- Establish software provider evaluation criteria.

Utilize the product experience: capability and platform with support for adaptability, manageability, reliability and usability, and the customer experience in TCO/ROI and Validation.

- Evaluate and select the software provider and products properly.

Apply a weighting the evaluation categories in the evaluation criteria to reflect your enterprise’s priorities to determine the short list of software providers and products.

- Establish the business initiative team to start the project.

Identify who will lead the project and the members of the team needed to plan and execute it with timelines, priorities and resources.

Using the ISG Buyers Guide and process provides enterprises a clear, structured approach to making smarter software and business investment decisions. It ensures alignment between strategy, people, processes and technology while reducing risk, saving time, and improving outcomes. The ISG approach promotes data-driven decision-making and collaboration, helping choose the right software providers for maximum value and return on investment.

Power and Utilities

The world’s population is expected to reach 9.7 billion by 2050, increasing global energy demand and accelerating the transformation of the power and utilities industry into a more diverse, digital and flexible system. As countries transform the energy infrastructure, utilities must balance rising consumption with clean-energy requirements, evolving regulations, supply chain constraints and geopolitical pressures. To maintain reliability, utilities must upgrade aging grids, improve operational efficiency, strengthen supply chain resilience and adopt advanced technologies such as artificial intelligence, digital twins and automation. With electrification expanding and distributed energy resources playing a larger role in generation and load management, the industry faces significant challenges and opportunities as it adapts to a rapidly changing energy landscape.

The industry faces significant challenges and opportunities as it adapts to a rapidly changing energy landscape.

ISG Research defines power and utilities software as an integrated ecosystem of platforms that support safe, reliable and efficient operation of generation, transmission and distribution networks. These platforms enable utilities to manage customer engagement, grid operations, field service, asset and equipment performance and predictive maintenance. By unifying operational and customer data, these systems improve visibility, strengthen reliability, streamline work execution and support regulatory and sustainability objectives across the utility value chain.

The power and utilities industry depends on complex, capital-intensive infrastructure that runs continuously to deliver safe and reliable service. These operations require coordinated maintenance, field service, customer engagement, grid oversight and real-time monitoring to ensure stability across transmission and distribution systems. Software platforms enhance visibility, streamline workflows and strengthen performance across these diverse environments. Customer engagement tools improve communication and service interactions, while digital twins, asset management and predictive maintenance platforms support real-time assessment of asset health, reduce maintenance costs and extend equipment life. Field service tools improve scheduling, dispatch and technician enablement, and grid management systems enhance outage response and overall system performance. Together, these platforms help utilities improve safety, efficiency and service delivery while managing evolving operational and regulatory demands.

Key software domains form a connected ecosystem that supports the end-to-end operation of power and utilities networks. Digital twins create virtual representations of power plants, substations and grid assets that support monitoring, analytics, maintenance and scenario modeling. Enterprise asset management systems guide asset lifecycles, maintenance, labor, controls and supply chain processes to improve reliability and reduce operational risk. Field service management equips technicians with the tools, communication channels and information required to execute work safely and efficiently across distributed service territories. Predictive maintenance combines condition monitoring, analytics and machine learning to identify early signs of equipment degradation and optimize maintenance planning. When combined, these platforms help utilities manage operational complexity, strengthen safety and reliability and improve performance across generation, transmission and distribution.

The power and utilities industry relies on a vast network of infrastructure that must operate continuously in demanding conditions. Power plants, substations, transmission lines and distribution grids require constant monitoring, maintenance and operational support to maintain a stable energy supply. As renewable penetration increases and weather patterns intensify, utilities must respond more quickly to grid stress, equipment failures and changing load conditions while maintaining service quality and regulatory compliance.

Utilities must respond quickly to grid stress, equipment failures and changing load conditions while maintaining service quality.

The industry has shifted from manual processes, siloed data and reactive maintenance toward a digitally connected operational landscape shaped by rising customer expectations, aging infrastructure, increasing system complexity and workforce shortages. Earlier customer engagement, field service and asset management workflows were largely transactional and lacked real-time insight. As operational pressures increased, utilities adopted advanced technologies, progressing from basic supervisory systems to integrated platforms that use AI, IoT data, cloud architectures, mobile applications, augmented reality and digital twins. These platforms have transformed essential functions into predictive, data-driven and increasingly automated capabilities. The industry continues to advance toward proactive operations that improve reliability, reduce cost, strengthen safety and compliance and enhance long-term resilience.

Utilities evaluating next-generation operational technologies across customer engagement, asset management, field service, grid operations, digital twins and predictive maintenance need platforms that streamline workflows, reduce manual effort and deliver measurable efficiency gains. This requires systems that strengthen reliability with proactive and predictive insights, provide real-time visibility into customers, assets and grid conditions and reduce downtime by improving scheduling, resource allocation and maintenance planning. These platforms must also support sustainability by reducing paper use, limiting truck rolls and fuel consumption, optimizing energy use and enabling greater integration of distributed resources. Above all, utilities should select providers that improve safety, strengthen performance and enable a more data-driven, future-ready operation.

Software in the power and utilities industry must deliver unified and intelligent capabilities that support asset management, field operations, customer engagement, grid oversight, digital twins and predictive maintenance. These platforms must streamline communication and maintenance workflows, reduce manual effort and provide real-time visibility into customers, assets and system conditions. Leading platforms incorporate proactive and predictive insights powered by AI, IoT data, cloud technologies and digital twins to improve reliability, minimize downtime and optimize resource allocation. They must also support sustainability and compliance by reducing unnecessary truck rolls, improving energy use, tracking emissions and enabling efficient system operations. Ultimately, successful platforms strengthen customer satisfaction and support field and operations teams while positioning the enterprise for a more efficient and future-ready utility environment.

Leading platforms incorporate proactive and predictive insights to improve reliability, minimize downtime and optimize resource allocation.

Enterprises in the power and utilities sector should select software providers that support the organization’s transition from reactive and siloed operations to integrated, predictive and data-driven environments. This requires prioritizing platforms that simplify communication and operational workflows, reduce manual effort and deliver measurable efficiency gains across customer engagement, asset lifecycle and performance management, field service, grid operations, digital twins and predictive maintenance. Providers must offer strong capabilities in real-time visibility, proactive and predictive insights, resource optimization and seamless integration across systems. They must also strengthen safety, reliability and compliance while supporting sustainability through reduced truck rolls, optimized energy use and improved emissions tracking. By selecting providers that combine AI, IoT, cloud technology, digital twins and analytics within cohesive and user-friendly platforms, utilities can maximize asset performance, enhance customer experience and future-proof operations in a rapidly evolving industry.

The 2025 ISG Buyers Guide™ for Power and Utilities evaluates 8 software providers in key areas that include customer engagement with experience and service support, enterprise asset management or asset performance management with collaboration, management and operations; field service with mobile support, scheduling and dispatch optimization, work order management and workforce management; and predictive and proactive maintenance support. Evaluate for platform support for analytics, data, devices, integration and knowledge management as well as AI support and investment. This research evaluates the following providers: Fluentgrid, GE Vernova, IBM, IFS, KloudGin, Oracle, PTC and SAP.

Key Takeaways

The power and utilities sector is undergoing a transition toward more digital, connected and predictive operations as providers transform aging infrastructure and respond to rising energy demand, distributed resources and increasing regulatory pressures. Utilities continue to integrate customer engagement, field operations, asset lifecyle and performance management and grid oversight as part of a unified operational framework supported by AI, IoT and digital twins. These shifts reflect the industry's movement from siloed, reactive workflows to platforms that enable proactive management and improved reliability.

Software Provider Summary

The ISG Buyers Guide™ for Power and Utilities evaluates eight software providers that offer products supporting enterprise asset management or asset performance management, field service, customer engagement and related platform capabilities for analytics, integration and AI. The research ranked the top three overall leaders as GE Vernova, Oracle and IFS. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. GE Vernova, IFS, Oracle and SAP were rated as Exemplary. Fluentgrid, IBM, KloudGin and PTC were rated as Merit.

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (30%) and Platform (50%), which includes adaptability, manageability, reliability and usability. GE Vernova, Oracle and IFS achieved the highest performance as Leaders in this category, supported by the breadth and depth of functional coverage across power and utilities requirements and robust platform foundations emphasizing adaptability, manageability, reliability and usability. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

Customer Experience, which accounts for 20% of the evaluation, focuses on validation and TCO/ROI. GE Vernova, Oracle and IFS were the Leaders in this category, showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should prioritize platforms that simplify operational workflows, strengthen safety and reliability and provide unified visibility across customer, asset and grid domains. Buyers should evaluate providers on the ability to deliver predictive insights, seamless integration and operational efficiency gains. Organizations should select platforms that support regulatory alignment, sustainability goals and long-term transformation of utility operations.

The Findings – Power and Utilities

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

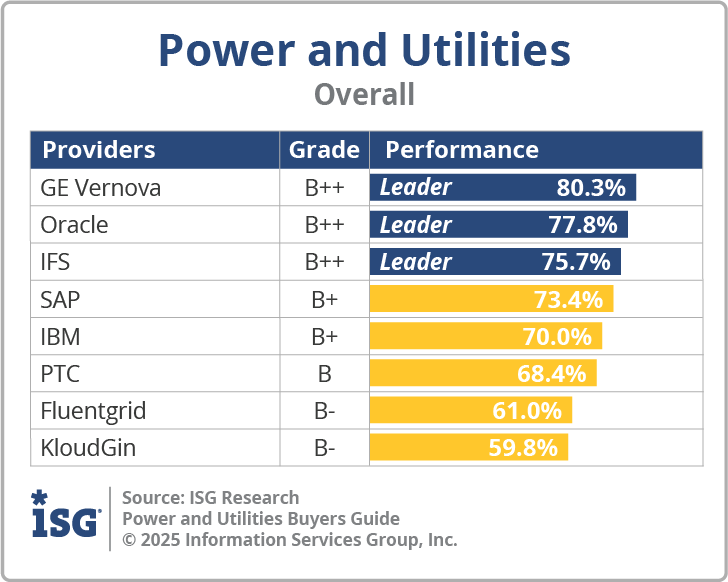

Overall Scoring of Software Providers Across Categories

The research finds GE Vernova atop the list, followed by Oracle and IFS. Providers that place in the top three of a category earn the designation of Leader. GE Vernova, IFS and Oracle have done so in five categories.

The research finds GE Vernova atop the list, followed by Oracle and IFS. Providers that place in the top three of a category earn the designation of Leader. GE Vernova, IFS and Oracle have done so in five categories.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: GE Vernova, IFS, Oracle and SAP.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. No providers are rated Innovative.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. No providers are rated Assurance.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: Fluentgrid, IBM, KloudGin and PTC.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

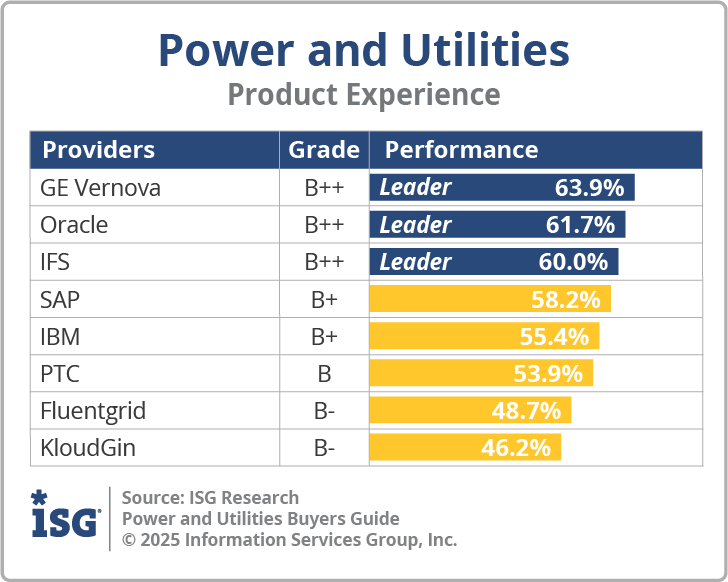

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (30%) and Platform (50%). GE Vernova, Oracle and IFS were designated Product Experience Leaders.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

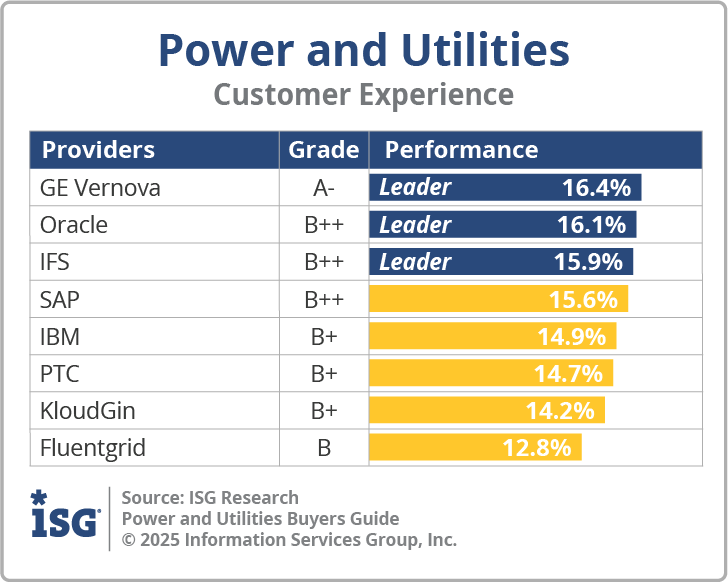

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are GE Vernova, Oracle and IFS. These category leaders best communicate commitment and dedication to customer needs.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Power and Utilities

For inclusion in the ISG Buyers Guide™ for overall Power and Utilities in 2025, a software provider must be in good standing financially and ethically, have at least $25 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents, and have at least 25 customers. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

All software providers that offer relevant products and meet the inclusion requirements are invited to participate in the Buyers Guide evaluation process, at no cost to them. If a provider does not respond to or decline the invitation, a determination is made whether to include it in our analysis based on our defined set of inclusion criteria. These criteria are designed to ensure we include in our evaluation providers’ geographic operations, customer base and revenue as well as all relevant aspects of the products’ fit for the particular category being evaluated.

If a provider is actively marketing, selling and developing a product as reflected on its website that is within the scope of the Buyers Guide, it is automatically evaluated for inclusion. We have adopted this approach because we view it as our responsibility to assess all relevant providers whether or not they choose to actively participate.

Software providers with defined functionality are evaluated on the ability to offer a combination (if not all) of the following capabilities:

-

Customer engagement (required)

-

Digital twin

-

Enterprise asset management or asset performance management (required)

-

Field service (required)

-

Predictive maintenance (required)

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer application suites or packages of products that may include relevant individual modules or applications.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| Fluentgrid | CRM, CSS, DSM, FMS, MWM, OCC, OMS, SMOC | N/A | December 2025 |

| GE Vernova | Asset Performance Management, APM Integrity Mobile, APM Rounds Pro, Autonomous Inspection, GridOS ADMS, GridOS AEMS, GridOS DERM, GridOS Field, GridOS Orchestration Software, GridOS Visual Intelligence, GridOS Geo Network Management, GridOS Data Fabric, Mobile Enterprise Suite, Proficy CSense, SmartSignal |

V5.3.x 1.5.1 |

December 2025 |

| IBM | Maximo Application Suite, Maximo Collaborate, Maximo Field Service Management, Maximo EAM, Maximo IoT, Maximo Manage, Maximo Mobile, Monitor and Health, Maximo Oil and Gas, Maximo Optimizer, Maximo Predict, Maximo Utilities |

9.2 8.0 |

November 2025 |

| IFS | Cloud EAM, Copperleaf, Field Service Management, Ultimo EAM |

25R2 24.4 |

November 2025 December 2024 |

| KloudGin | Core | N/A | December 2025 |

| Oracle | Fusion Cloud SCM, Fusion Field Service, IoT, Utilities Opower Cloud | 26A 25.10 |

December 2025 November 2025 September 2025 |

| PTC |

ThingWorx Industrial IoT Platform, ThingWorx Analytics, ThingWorx Applications, ThingWorx Predictive, Maintenance, Service Board, ServiceMax AI, ServiceMax Core, ServiceMax FieldFX, ServiceMax Go, ServiceMax Asset 360 for Salesforce |

10.0 25R2 / 25.2 13.0 4.0 12 |

December 2025 |

| SAP | Intelligent Asset Management, Aset Performance Management, Field Service Management, Industry Solution for Utilities, S/4 HANA Cloud, S/4 HANA Utilities, Utilities Core | 2511 | November 2025 |

Providers of Promise

We did not include software providers that, as a result of our research and analysis, did not satisfy the criteria for inclusion in this Buyers Guide. These are listed below as “Providers of Promise.”

| Provider | Product | Capability | Customers | Geography | Revenue | |

|---|---|---|---|---|---|---|

| AspenTech | APM, Aspen Mtell, OSI ADMS, OSI GMS | No | Yes | Yes | Yes | |

| CGI | Production Management Suite. OpenGrid Field | No | Yes | Yes | Yes | |

| Hexagon | HxGN APM, HxGN EAM, HxGN EAM Digital Work, HxGM NetWorks, HxGN SDx. | No | Yes | Yes | Yes | |

| Hitachi Energy | APM, Asset Suite EAM, Ellipse EAM, Energy Portfolio Management, eSOMS, Lumada Asset and Work Management, Network Manager, Network SCADA and GMS, Service Suite. | No | Yes | Yes | Yes | |

| OverIT | NextGen FSM, NextGen Field Collaboration, NextGen Geo | No | Yes | Yes | Yes | |

| Ramco | EAM, ERP | No | Yes | Yes | Yes | |

Power and Utilities Customer Engagement

The power and utilities industry relies on complex, distributed operations that require coordinated customer engagement to maintain satisfaction and trust. Today’s customer engagement platforms support proactive communication, multi-channel service interactions and streamlined appointment scheduling for service-related needs. These capabilities improve response times, reduce service costs and create more customer-focused utility operations by providing better visibility into customer activity, scheduled visits, service events and communications.

Today’s customer engagement platforms support proactive communication, multi-channel service interactions and streamlined appointment scheduling.

ISG Research defines customer engagement in power and utilities as the set of capabilities that support omnichannel communication, automated notifications, self-service appointment booking and tracking, IVR, chat and virtual assistants, case and inquiry management, remote support tools, mobile applications, cloud services and integration with field service, billing and grid operations. These capabilities enable customers to manage appointments, receive updates, view service history, access remote assistance and personalize communication while helping service teams streamline workflows and maintain high-quality engagement.

Customer engagement is becoming more challenging as expectations for transparency and control rise, digital channels expand and service complexity increases. To address this, current platforms integrate AI, real-time data, IoT signals, mobile tools, augmented reality and digital twins to personalize interactions, automate updates, support remote resolution and improve the experiences of both customers and technicians.

Enterprises evaluating customer engagement software should prioritize platforms that streamline communication, support multi-channel scheduling and deliver measurable efficiency gains through improved visibility, reduced call volume and faster resolution. Advanced offerings enhance reliability with proactive insights, reduce environmental impact by minimizing paper use and truck rolls and improve satisfaction through timely communication and remote-assist tools that build long-term trust.

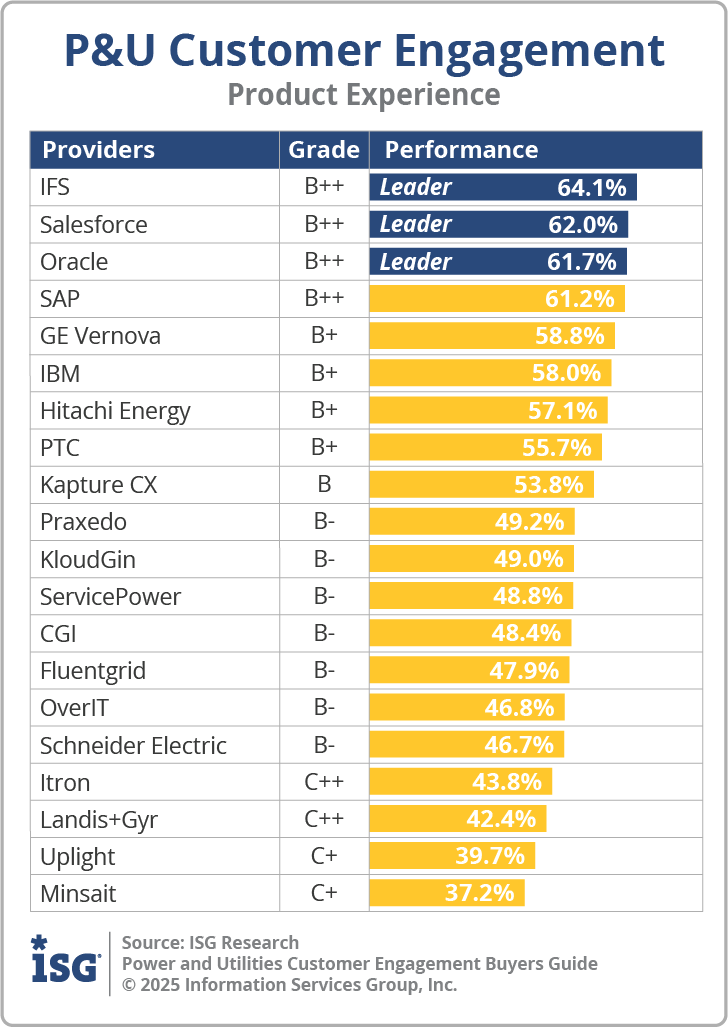

The 2025 ISG Buyers Guide™ for Customer Engagement evaluates 20 software providers in key areas including customer experience and service; built-in access to field service and predictive maintenance; industry-specific support; and platform support for analytics, data, devices, integration and knowledge management, AI support and investment. This research evaluates the following providers: CGI, Fluentgrid, GE Vernova, Hitachi Energy, IBM, IFS, Itron, Kapture CX, KloudGin, Landis+Gyr, Minsait, Oracle, OverIT, Praxedo, PTC, Salesforce, SAP, Schneider Electric, ServicePower and Uplight.

Key Takeaways

Customer engagement in power and utilities is shifting from transactional interactions to integrated platforms that provide real-time visibility and consistent, multi-channel communication. Utilities are adopting digital tools that streamline scheduling, automate updates and support self-service as customer expectations for transparency and control rise. These capabilities enable more proactive engagement, reduce operational burden and help teams manage growing service complexity.

Software Provider Summary

The ISG Buyers Guide™ for Power and Utilities Customer Engagement evaluates 20 software providers that offer capabilities supporting omnichannel communication, automated notifications, self-service appointment management, case handling, mobile applications and integration with field service and grid operations. The research ranked the top three overall leaders as IFS, Oracle and Salesforce. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. GE Vernova, Hitachi Energy, IBM, IFS, Oracle, PTC, Salesforce and SAP were rated as Exemplary, with Kapture CX, KloudGin and Praxedo rated as Innovative. CGI and Schneider Electric were rated as Assurance, and Fluentgrid, Itron, Landis+Gyr, Minsait, OverIT, ServicePower and Uplight were rated as Merit.

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (35%) and Platform (45%), including adaptability, manageability, reliability and usability. IFS, Salesforce and Oracle achieved the highest performance as Leaders in this category, supported by broad and deep customer engagement capabilities spanning scheduling, notifications, case handling and remote support and strong platform foundations, delivering reliable performance, intuitive usability and enterprise-grade adaptability. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

Customer Experience, representing 20% of the evaluation, focuses on validation and TCO/ROI. GE Vernova, Oracle and IFS were the Leaders in this category showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should prioritize platforms that unify customer communication, scheduling and case management while improving visibility and resolution efficiency. Buyers should emphasize providers that deliver predictive insights, multichannel engagement, AI-enabled support and seamless integration with field service and grid operations. Organizations should select software that strengthens reliability, reduces operational burden and supports sustainability objectives through more efficient, digitally enabled customer interactions.

The Findings – Power and Utilities Customer Engagement

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

Overall Scoring of Software Providers Across Categories

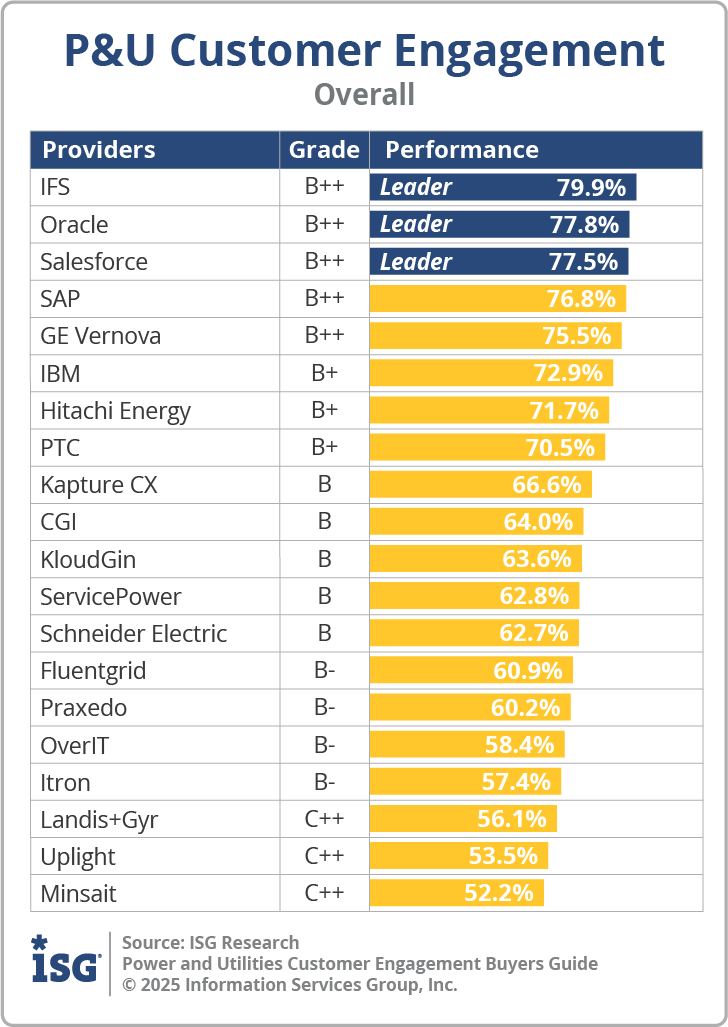

The research finds IFS atop the list, followed by Oracle and Salesforce. Providers that place in the top three of a category earn the designation of Leader. IFS and Oracle have done so in five categories; Salesforce in three and GE Vernova in two categories.

The research finds IFS atop the list, followed by Oracle and Salesforce. Providers that place in the top three of a category earn the designation of Leader. IFS and Oracle have done so in five categories; Salesforce in three and GE Vernova in two categories.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: GE Vernova, Hitachi Energy, IBM, IFS, Oracle, PTC, Salesforce and SAP.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The providers rated Innovative are: Kapture CX, KloudGin and Praxedo.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The providers rated Assurance are: CGI and Schneider Electric.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: Fluentgrid, Itron, Landis+Gyr, Minsait, OverIT, ServicePower and Uplight.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (35%) and Platform (45%). IFS, Salesforce and Oracle were designated Product Experience Leaders.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are GE Vernova, Oracle and IFS. These category leaders best communicate commitment and dedication to customer needs.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Power and Utilities Customer Engagement

For inclusion in the ISG Buyers Guide™ for overall Power and Utilities Customer Engagement in 2025, a software provider must be in good standing financially and ethically, have at least $25 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents, and have at least 25 customers. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

All software providers that offer relevant products and meet the inclusion requirements are invited to participate in the Buyers Guide evaluation process, at no cost to them. If a provider does not respond to or decline the invitation, a determination is made whether to include it in our analysis based on our defined set of inclusion criteria. These criteria are designed to ensure we include in our evaluation providers’ geographic operations, customer base and revenue as well as all relevant aspects of the products’ fit for the particular category being evaluated.

If a provider is actively marketing, selling and developing a product as reflected on its website that is within the scope of the Buyers Guide, it is automatically evaluated for inclusion. We have adopted this approach because we view it as our responsibility to assess all relevant providers whether or not they choose to actively participate.

Software providers with defined functionality are evaluated on the ability to offer a combination (if not all) of the following capabilities:

-

Customer engagement (required)

-

Service and experience

-

-

Access to field service

-

Access to predictive maintenance

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer application suites or packages of products that may include relevant individual modules or applications.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| CGI | OpenGrid Field, OpenGrid Integrated Network Model, OpenGrid Network | N/A | December 2025 |

| Fluentgrid | CRM, CSS, DSM, FMS, MWM, OCC, OMS, SMOC | N/A | December 2025 |

| GE Vernova | Asset Performance Management, APM Integrity Mobile, APM Rounds Pro, Autonomous Inspection, GridOS ADMS, GridOS AEMS, GridOS DERM, GridOS Field, GridOS Orchestration Software, GridOS Visual Intelligence, GridOS Geo Network Management, GridOS Data Fabric, Mobile Enterprise Suite, Proficy CSense, SmartSignal |

V5.3.x 1.5.1 |

December 2025 |

| Hitachi Energy | APM, Asset Suite EAM, Ellipse EAM, Energy Portfolio Management, eSOMS, Lumada Asset and Work Management, Network Manager, Network SCADA and GMS, Service Suite. | N/A | December 2025 |

| IBM | Maximo Application Suite, Maximo Collaborate, Maximo Field Service Management, Maximo EAM, Maximo IoT, Maximo Manage, Maximo Mobile, Monitor and Health, Maximo Oil and Gas, Maximo Optimizer, Maximo Predict, Maximo Utilities |

9.2 8.0 |

November 2025 |

| IFS | Cloud EAM, Copperleaf, Field Service Management, Ultimo EAM |

25R2 24.4 |

November 2025 December 2024 |

| Itron | IntelliSOURCE Customer, Analytics – Customer Portal | N/A | December 2025 |

| Kapture | CX | N/A | December 2025 |

| KloudGin | Core | N/A | December 2025 |

| Landis+Gyr | SmartData Connect | N/A | December 2025 |

| Minsait | Onesait Utilities Customers | N/A | December 2025 |

| Oracle | Fusion Cloud SCM, Fusion Field Service, IoT, Utilities Opower Cloud | 26A 25.10 |

December 2025 November 2025 September 2025 |

| OverIT | NextGen FSM, NextGen Field Collaboration, NextGen Geo | N/A | December 2025 |

| PTC |

ThingWorx Industrial IoT Platform, ThingWorx Analytics, ThingWorx Applications, ThingWorx Predictive, Maintenance, Service Board, ServiceMax AI, ServiceMax Core, ServiceMax FieldFX, ServiceMax Go, ServiceMax Asset 360 for Salesforce |

10.0 25R2 / 25.2 13.0 4.0 12 |

December 2025 |

| Praxedo | Praxedo | N/A | December 2025 |

| Salesforce | Asset Service Lifecycle Management, Field Service, Energy & Utilities Cloud | Winter 2026 | October 2025 |

| SAP | Intelligent Asset Management, Aset Performance Management, Field Service Management, Industry Solution for Utilities, S/4 HANA Cloud, S/4 HANA Utilities, Utilities Core | 2511 | November 2025 |

| Schneider Electric | One Digital Grid Platform | N/A | December 2025 |

| ServicePower | Field Service Management Platform | N/A | December 2025 |

| Uplight | Platform | N/A | December 2025 |

Providers of Promise

We did not include software providers that, as a result of our research and analysis, did not satisfy the criteria for inclusion in this Buyers Guide. These are listed below as “Providers of Promise.”

| Provider | Product | Capability | Customers | Geography | Revenue |

|---|---|---|---|---|---|

| AspenTech | Grid Apps | No | Yes | Yes | Yes |

| Microsoft | Dynamics 365 Customer Engagement | No | Yes | Yes | Yes |

| Nexgrid | Platform | No | Yes | Yes | Yes |

| OATI | webSmartView | No | Yes | Yes | Yes |

| Siemens | Energy Engage Mobile | No | Yes | Yes | Yes |

| Survalent | SurvalentONE OMS | No | Yes | Yes | Yes |

| Tantalus | SmartWorks Customer Engagement | No | Yes | Yes | Yes |

Power and Utilities Digital Twin

The power and utilities industry depends on complex, always-running infrastructure that requires real-time insight to maintain safety, reliability and productivity. Digital twin technology supports these needs by creating dynamic virtual models of physical assets, enabling utilities to monitor conditions, track performance and predict issues across the asset lifecycle. With better visibility, digital twins improve asset performance, reduce maintenance costs and help operators maintain safe, efficient operations.

ISG Research defines digital twins in the power and utilities industry as virtual representations of physical assets that support lifecycle management, maintenance, repair and operations, workforce coordination, controls management, application support, supply chain processes, cloud-based analytics, asset health monitoring, digital enablement services and remote operations. They provide a data-driven view of asset condition and behavior, using insights, simulation tools and predictive intelligence to extend asset life and reduce operational costs.

Digital twins help extend asset life and reduce operational costs.

Digital twin adoption is accelerating as infrastructure ages, operating conditions grow more severe and experienced personnel retire. Utilities are turning to current platforms that use AI, IoT data, cloud systems, mobile tools and augmented reality to build real-time predictive models that optimize maintenance, strengthen field operations and support sustainability and regulatory reporting. These capabilities help utilities meet rising expectations for safety, performance and compliance while improving the management of distributed assets.

Enterprises evaluating digital twin providers should prioritize platforms that streamline maintenance workflows, reduce manual effort and deliver measurable efficiency and cost gains through improved asset visibility and reduced downtime. Advanced offerings enhance reliability with predictive insights powered by real-time data and simulation, and support sustainability by modeling energy use, tracking emissions and identifying opportunities to reduce environmental impact. Selecting providers with these capabilities helps utilities improve operations and long-term performance.

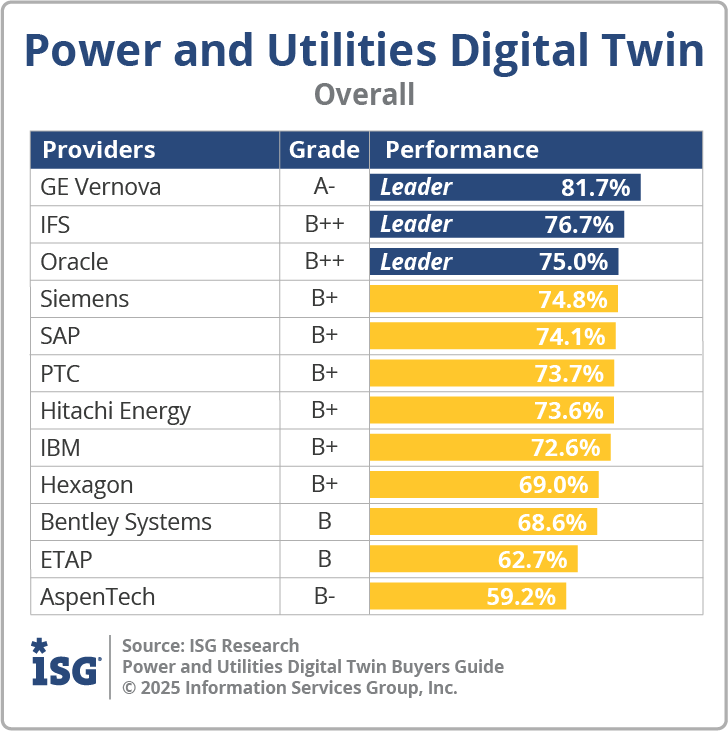

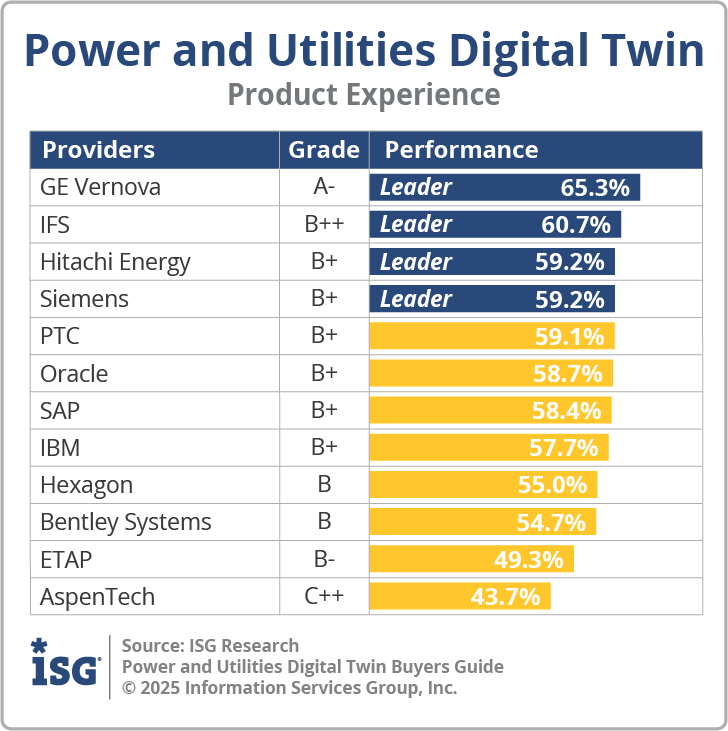

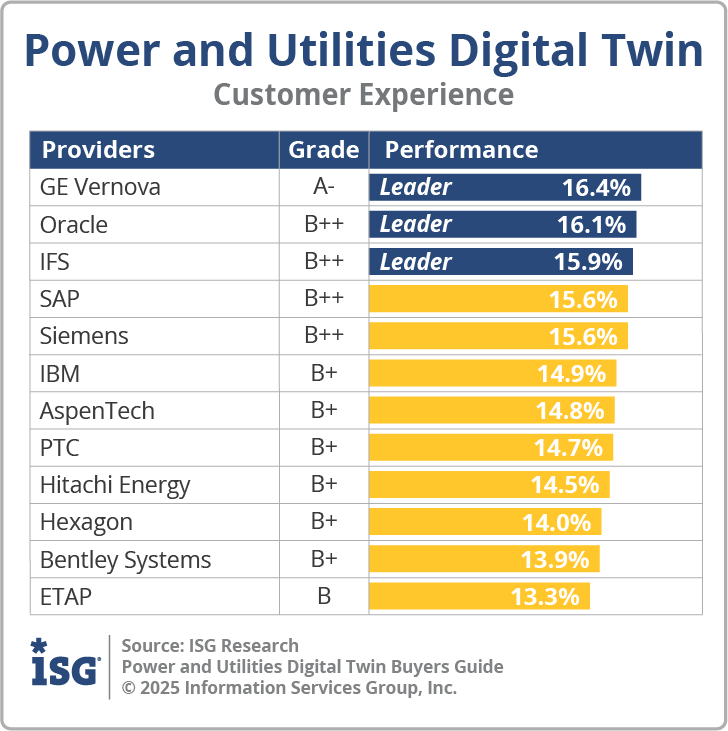

The 2025 ISG Buyers Guide™ for Digital Twin evaluates 12 software providers in key areas that include support for asset modeling, integration, performance, visualization and ecosystem enablement; access to assets, grid and predictive maintenance; industry-specific functionality; and platform support for analytics, data, devices, integration and knowledge management, AI support and investment. This research evaluates the following providers: AspenTech, Bentley Systems, ETAP, GE Vernova, Hexagon, Hitachi Energy, IBM, IFS, Oracle, PTC, SAP and Siemens.

Key Takeaways

Digital twin adoption in power and utilities is expanding as operators seek real-time visibility, predictive insight and more efficient management of aging and distributed assets. Advanced platforms unify asset condition monitoring, simulation and predictive intelligence to improve maintenance, strengthen field operations and support compliance needs. These capabilities help utilities reduce manual effort, improve operational reliability and better manage increasingly complex infrastructure.

Software Provider Summary

The ISG Buyers Guide™ for Digital Twin evaluates 12 software providers offering platforms that support asset modeling, performance monitoring, integration, visualization and predictive operations. The research ranked the top three overall leaders as GE Vernova, IFS and Oracle. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. GE Vernova, IFS, Oracle and Siemens were rated as Exemplary, with Hitachi Energy and PTC rated as Innovative. AspenTech, IBM and SAP were rated as Assurance, and Bentley Systems, ETAP and Hexagon were rated as Merit.

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (35%) and Platform (45%), including adaptability, manageability, reliability and usability. GE Vernova, IFS and Hitachi Energy achieved the highest performance as Leaders in this category, supported by broad and deep digital twin capabilities across asset lifecycle monitoring and predictive modeling and strong underlying platform foundations emphasizing adaptability, reliability, usability and enterprise-grade manageability. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

Customer Experience, representing 20% of the evaluation, focuses on validation and TCO/ROI. GE Vernova, Oracle and IFS were the Leaders in this category showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should prioritize digital twin platforms that streamline maintenance workflows, strengthen operational visibility and support predictive, data-driven decision-making. Buyers should emphasize capabilities that integrate real-time data, simulation and analytics while supporting interoperability across asset management, field operations and grid systems. Organizations should select providers that enhance reliability, reduce operational burden and align digital twin investments with long-term performance and sustainability objectives.

The Findings – Power and Utilities Digital Twin

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

Overall Scoring of Software Providers Across Categories

The research finds GE Vernova atop the list, followed by IFS and Oracle. Providers that place in the top three of a category earn the designation of Leader. GE Vernova has done so in five categories, IFS in four, Oracle in three, Hitachi Energy in two and PTC in one category.

The research finds GE Vernova atop the list, followed by IFS and Oracle. Providers that place in the top three of a category earn the designation of Leader. GE Vernova has done so in five categories, IFS in four, Oracle in three, Hitachi Energy in two and PTC in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: GE Vernova, IFS, Oracle and Siemens.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The providers rated Innovative are: Hitachi Energy and PTC.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The providers rated Assurance are: AspenTech, IBM and SAP.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: Bentley Systems, ETAP and Hexagon.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (35%) and Platform (45%). GE Vernova, IFS, Hitachi Energy and Siemens were designated Product Experience Leaders. While not Leaders, PTC and Oracle were also found to meet a broad range of enterprise product experience requirements.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are GE Vernova, Oracle and IFS. These category leaders best communicate commitment and dedication to customer needs.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Power and Utilities Digital Twin

For inclusion in the ISG Buyers Guide™ for overall Power and Utilities Digital Twin in 2025, a software provider must be in good standing financially and ethically, have at least $25 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents, and have at least 25 customers. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

All software providers that offer relevant products and meet the inclusion requirements are invited to participate in the Buyers Guide evaluation process, at no cost to them. If a provider does not respond to or decline the invitation, a determination is made whether to include it in our analysis based on our defined set of inclusion criteria. These criteria are designed to ensure we include in our evaluation providers’ geographic operations, customer base and revenue as well as all relevant aspects of the products’ fit for the particular category being evaluated.

If a provider is actively marketing, selling and developing a product as reflected on its website that is within the scope of the Buyers Guide, it is automatically evaluated for inclusion. We have adopted this approach because we view it as our responsibility to assess all relevant providers whether or not they choose to actively participate.

Software providers with defined functionality are evaluated on the ability to offer a combination (if not all) of the following capabilities:

-

Digital twin (required)

-

Modeling and simulation

-

Integration and IoT

-

Asset performance and predictive

-

Lifecycle and asset performance

-

Visualization and collaboration

-

-

Access to EAM or APM

-

Access to predictive maintenance

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer application suites or packages of products that may include relevant individual modules or applications.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| AspenTech | APM, Aspen Mtell, OSI ADMS, OSI GMS |

4.0 V15 |

May 2025 |

| Bentley Systems | AssetWise, iTwin, OpenPlant, OpenUtilities, PlantSight, SACS SPIDAstudio. |

6.0 25.0.2 V3.0 |

October 2025 February 2025 |

| Fluentgrid | CRM, CSS, DSM, FMS, MWM, OCC, OMS, SMOC | N/A | December 2025 |

| GE Vernova | Asset Performance Management, APM Integrity Mobile, APM Rounds Pro, Autonomous Inspection, GridOS ADMS, GridOS AEMS, GridOS DERM, GridOS Field, GridOS Orchestration Software, GridOS Visual Intelligence, GridOS Geo Network Management, GridOS Data Fabric, Mobile Enterprise Suite, Proficy CSense, SmartSignal |

V5.3.x 1.5.1 |

December 2025 |

| Hexagon | HxGN APM, HxGN EAM, HxGN EAM Digital Work, HxGM NetWorks, HxGN SDx. | 12.3 | December 2025, November 2025, February 2025 |

| Hitachi Energy | APM, Asset Suite EAM, Ellipse EAM, Energy Portfolio Management, eSOMS, Lumada Asset and Work Management, Network Manager, Network SCADA and GMS, Service Suite. | N/A | December 2025 |

| IBM | Maximo Application Suite, Maximo Collaborate, Maximo Field Service Management, Maximo EAM, Maximo IoT, Maximo Manage, Maximo Mobile, Monitor and Health, Maximo Oil and Gas, Maximo Optimizer, Maximo Predict, Maximo Utilities |

9.2 8.0 |

November 2025 |

| IFS | Cloud EAM, Copperleaf, Field Service Management, Ultimo EAM |

25R2 24.4 |

November 2025 December 2024 |

| Oracle | Fusion Cloud SCM, Fusion Field Service, IoT, Utilities Opower Cloud | 26A 25.10 |

December 2025 November 2025 September 2025 |

| PTC |

ThingWorx Industrial IoT Platform, ThingWorx Analytics, ThingWorx Applications, ThingWorx Predictive, Maintenance, Service Board, ServiceMax AI, ServiceMax Core, ServiceMax FieldFX, ServiceMax Go, ServiceMax Asset 360 for Salesforce |

10.0 25R2 / 25.2 13.0 4.0 12 |

December 2025 |

| SAP | Intelligent Asset Management, Aset Performance Management, Field Service Management, Industry Solution for Utilities, S/4 HANA Cloud, S/4 HANA Utilities, Utilities Core | 2511 | November 2025 |

| Siemens | COMOS, Topsides, Xcelerator | N/A | December 2025 |

Providers of Promise

We did not include software providers that, as a result of our research and analysis, did not satisfy the criteria for inclusion in this Buyers Guide. These are listed below as “Providers of Promise.”

| Provider | Product | Capability | Customers | Geography | Revenue |

|---|---|---|---|---|---|

| ABB | Ability SafetyInsight | No | Yes | Yes | Yes |

| ETAP | ETAP | No | Yes | Yes | Yes |

| Microsoft | Azure Digital Twins | No | Yes | Yes | Yes |

| Schneider Electric | DORIS Group, AVEVA | No | Yes | Yes | Yes |

Power and Utilities EAM

The power and utilities industry relies on complex, always-running infrastructure that requires strong asset management to ensure safety, reliability and productivity. Enterprise asset management (EAM) ) or asset performance management (APM) software helps utilities monitor and maintain assets throughout their lifecycle, improving performance, reducing maintenance costs and supporting environmentally responsible operations. By providing better visibility, streamlined processes and more informed decision-making, EAM and APM systems help maximize uptime, control costs and keep utility operations running efficiently.

ISG Research defines EAM in the power and utilities industry as software that enables asset lifecycle management, maintenance, repair and operations, labor and controls management, application maintenance, supply chain activity, cloud services, asset health monitoring, digital enablement and remote oversight. These capabilities increase asset performance, extend asset life and reduce operational costs while giving management and operators better operational insight.

Managing utility assets is becoming more challenging as infrastructure ages, environments grow harsher and skilled expertise declines.

Managing utility assets is becoming more challenging as infrastructure ages, environments grow harsher and skilled expertise declines. These pressures are driving the adoption of more advanced EAM and APM platforms that improve reliability, reduce costs and support interconnected operations. Newer systems combine AI, IoT data, cloud architectures, mobile tools, augmented reality and digital twins to enable predictive maintenance, strengthen field service, extend asset lifecycles and support sustainability reporting. This convergence of technologies is shaping the market by providing the insight needed to meet rising performance, safety and compliance expectations.

Enterprises evaluating EAM and APM providers should prioritize platforms that streamline maintenance, reduce manual work and deliver measurable efficiency and cost benefits through improved asset utilization and reduced downtime. Today’s EAM offerings enhance reliability with predictive insights and support sustainability by tracking carbon impacts and optimizing energy use, helping utilities strengthen operations and long-term performance.

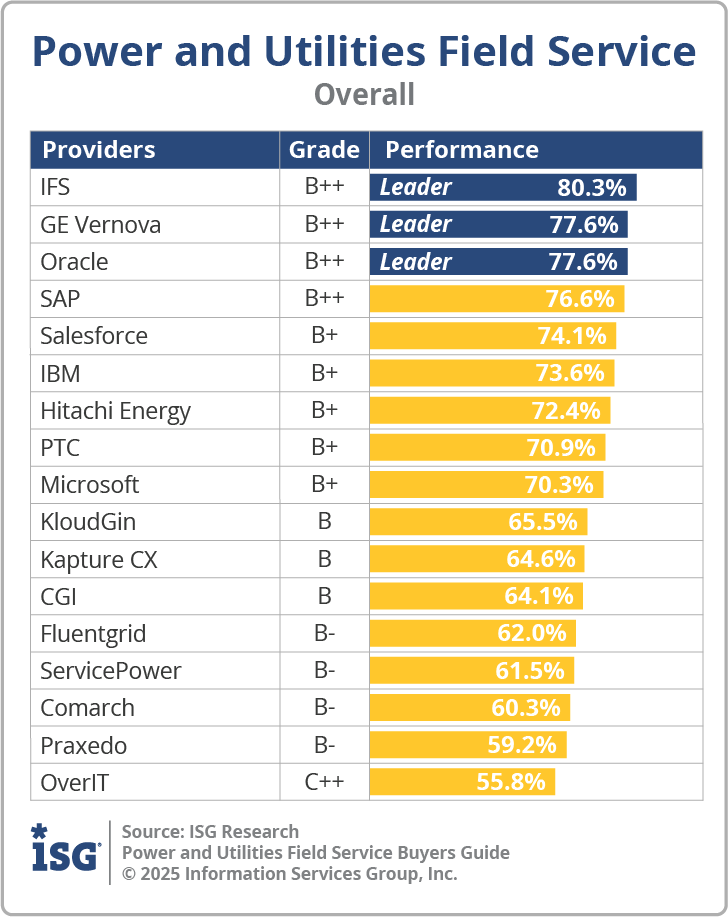

The 2025 ISG Buyers Guide™ for Enterprise Asset Management evaluates 14 software providers in key areas that include support for collaboration, management, operations and performance; access to digital twins and predictive maintenance; industry-specific functionality; and platform support for analytics, data, devices, integration and knowledge management, AI support and investment. This research evaluates the following providers: AspenTech, AssetWorks, Bentley Systems, Fluentgrid, GE Vernova, Hexagon, Hitachi Energy, IBM, IFS, KloudGin, Oracle, PTC, Ramco and SAP.

Key Takeaways

Enterprise asset management in power and utilities is evolving from manual and reactive maintenance into more connected, data-driven and predictive operations. Today’s EAM and APM platforms unify asset visibility, maintenance workflows and operational insight to strengthen reliability and improve decision-making across distributed infrastructure. These capabilities help utilities manage aging assets, reduce operational burden and support long-term performance and compliance expectations.

Software Provider Summary

The ISG Buyers Guide™ for Enterprise Asset Management evaluates 14 software providers that offer capabilities supporting asset lifecycle management, maintenance, operations, digital twins, performance, predictive maintenance and platform functions for analytics, integration and AI. The research ranked the top three overall leaders as GE Vernova, IFS and Oracle. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. GE Vernova, IBM, IFS, Oracle, PTC and SAP were rated as Exemplary, with Hitachi Energy rated as Innovative. AspenTech was rated as Assurance, and AssetWorks, Bentley Systems, Fluentgrid, Hexagon, KloudGin and Ramco were rated as Merit.

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (35%) and Platform (45%), including adaptability, manageability, reliability and usability. IFS, GE Vernova and Oracle achieved the highest performance as Leaders in this category, supported by broad and deep EAM or APM capabilities spanning lifecycle management, predictive maintenance, asset collaboration and digital twin integration and strong underlying platform foundations emphasizing reliability, usability, adaptability and enterprise-grade manageability. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

Customer Experience, which accounts for 20% of the evaluation, focuses on validation and TCO/ROI. GE Vernova, Oracle and IFS were the Leaders in this category, showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should prioritize EAM platforms that streamline maintenance workflows, reduce manual effort and strengthen visibility into asset condition and performance. Buyers should evaluate providers based on the ability to deliver predictive insights, integrate with digital twin and field operations systems and support scalable, secure and interoperable architectures. Organizations should adopt platforms that enhance operational reliability, reduce cost and align EAM investments with long-term sustainability and transformation objectives.

The Findings – Power and Utilities EAM

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

Overall Scoring of Software Providers Across Categories

The research finds GE Vernova atop the list, followed by IFS and Oracle. Providers that place in the top three of a category earn the designation of Leader. IFS and Oracle have done so in five categories, GE Vernova in four and Hitachi Energy in one category.

The research finds GE Vernova atop the list, followed by IFS and Oracle. Providers that place in the top three of a category earn the designation of Leader. IFS and Oracle have done so in five categories, GE Vernova in four and Hitachi Energy in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: GE Vernova, IBM, IFS, Oracle, PTC and SAP.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The provider rated Innovative is: Hitachi Energy.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The provider rated Assurance is: AspenTech.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: AssetWorks, Bentley Systems, Fluentgrid, Hexagon, KloudGin and Ramco.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (35%) and Platform (45%). IFS, GE Vernova and Oracle were designated Product Experience Leaders.

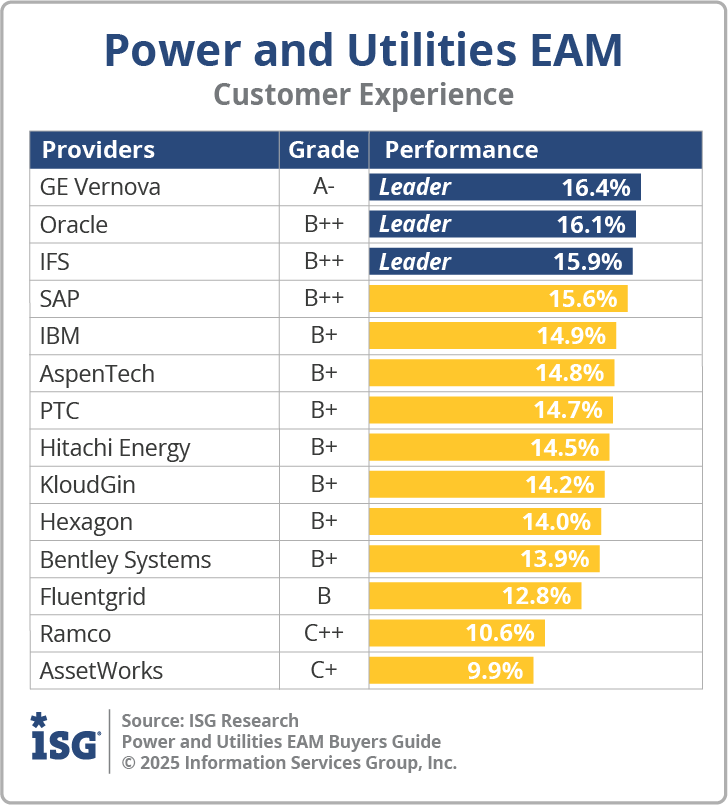

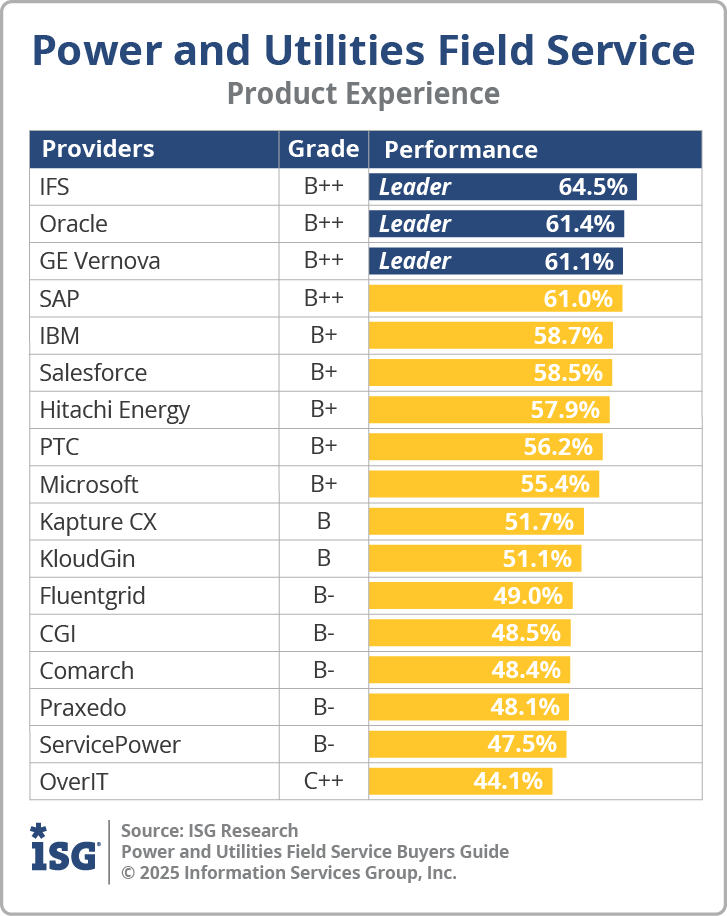

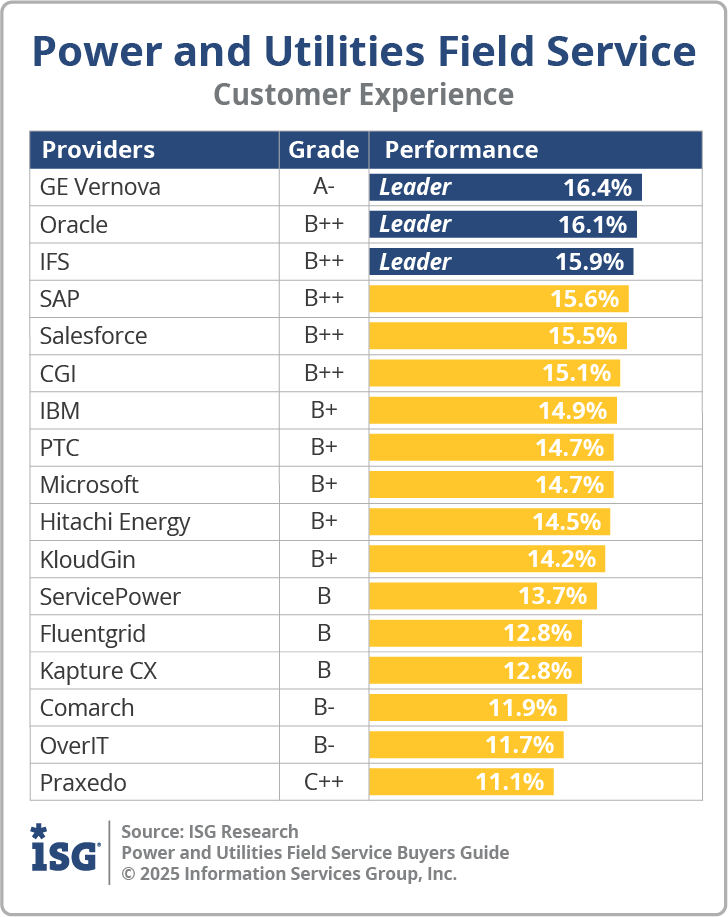

Customer Experience

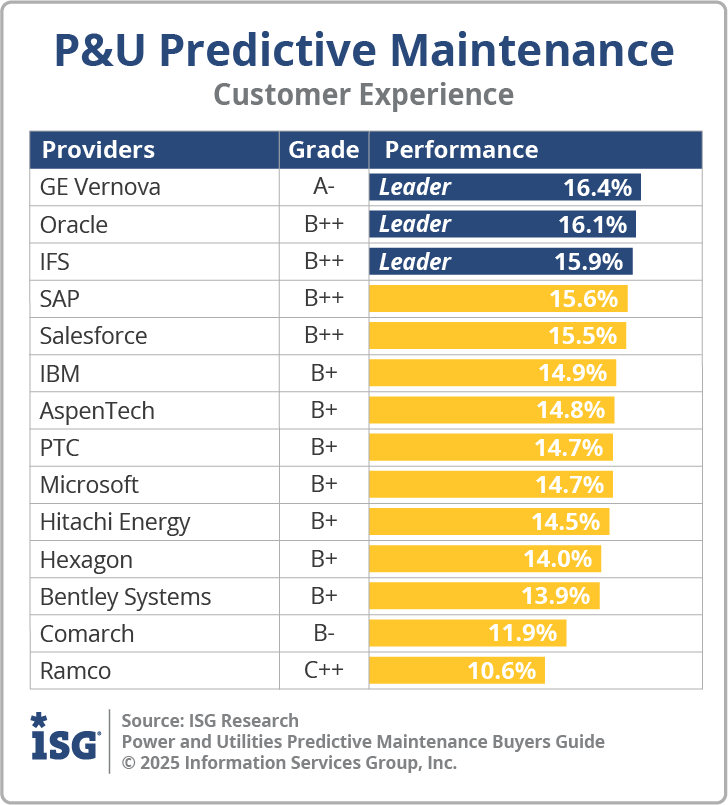

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.