Jeff Orr leads the firm’s overall research and advisory for CIO and technology leaders focused on the expertise of digital technology and the modernization and transformation for IT at ISG Software Research. Jeff’s coverage spans cloud computing, DevOps and platforms, digital security, intelligent automation, ITOps and service management, and observation technologies for intelligent automation. Jeff previously led the products team at Ventana Research providing educational and research insights. Prior to joining ISG and Ventana Research, he served as editor-in-chief and thought leader for Cyber Security Hub. Jeff spent a decade as a Research Director at ABI Research, and two decades as a technology, product and marketing leader. Jeff attended Embry-Riddle Aeronautical University, UC Berkeley and UC Santa Cruz. He is also an Oregon State University Certified Master Gardener.

narration area

Executive Summary

Buyers Guide Overview

ISG Research has conducted market research for over two decades across vertical industries, business applications, AI and IT. We have designed the ISG Buyers Guide™ to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements. Utilization of our research methodology and decades of experience enables our Buyers Guide to be an effective method to assess and select software providers and products. The findings of this research provide a comprehensive approach to rating software providers and rank their ability to meet specific product and customer experience requirements.

ISG Research has designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements.

The 2026 ISG Buyers Guides™ for Intelligent Automation Platforms Emerging Providers, covering Process Intelligence Platforms Emerging Providers, Intelligent Document Processing Platforms Emerging Providers and Automation and Orchestration Platforms Emerging Providers, are the distillation of continuous market and product research. It is an assessment of how well software providers’ offerings address enterprises’ requirements for intelligent automation software. The Value Index methodology is structured to support a request for information (RFI) for a request for proposal (RFP) process by incorporating all criteria needed to evaluate, select, utilize and maintain relationships with software providers. The ISG Buyers Guide evaluates customer experience and the product experience in its capability and platform.

The structure of the research reflects our understanding that the effective evaluation of software providers and products involves far more than just examining product features, potential revenue or customers generated from a provider’s marketing and sales efforts. It can ensure the best long-term relationship and value achieved from a resource and financial investment We believe it is important to take a comprehensive, research-based approach, since making the wrong choice of intelligent automation platform software can raise the total cost of ownership, lower the return on investment and hamper an enterprise’s ability to reach its potential. In addition, this approach can reduce the project’s development and deployment time and eliminate the risk of relying on opinions or historical biases.

ISG Research believes that an objective review of existing and potential new software providers and products is a critical strategy for the adoption and implementation of intelligent automation software. An enterprise’s review should include an analysis of both what is possible and what is relevant. We urge enterprises to do a thorough job of evaluating intelligent automation platforms and offer these Buyers Guides as both the results of our in-depth analysis of these providers and as an evaluation methodology.

How To Use This Buyers Guide

Evaluating Software Providers: The Process

We recommend using the Buyers Guide to assess and evaluate new or existing software providers for your enterprise. The market research can be used as an evaluation framework to assess existing approaches and software providers or establish a formal request for information from providers on products and customer experience and will shorten the cycle time when creating an RFI. The steps listed below provide a process that can facilitate best possible outcomes in the most efficient manner.

- Define the business case and goals.

Define the mission and business case for investment and the expected outcomes from your organizational and technological efforts. - Specify the business and IT needs.

Defining the business and IT requirements helps identify what specific capabilities are required with respect to people, processes, information and technology. - Assess the required roles and responsibilities.

Identify the individuals required for success at every level of the enterprise from executives to frontline workers and determine the needs of each. - Outline the project’s critical path.

What needs to be done, in what order and who will do it? This outline should make clear the prior dependencies at each step of the project plan. - Ascertain the technology approach.

Determine the business and technology approach that most closely aligns to your enterprise’s requirements. - Establish software provider evaluation criteria.

Utilize the product experience: capability and platform with support for adaptability, manageability, reliability and usability, and the customer experience in TCO/ROI and Validation. - Evaluate and select the software provider and products properly.

Apply a weighting the evaluation categories in the evaluation criteria to reflect your enterprise’s priorities to determine the short list of software providers and products. - Establish the business initiative team to start the project.

Identify who will lead the project and the members of the team needed to plan and execute it with timelines, priorities and resources.

Using the ISG Buyers Guide and process provides enterprises a clear, structured approach to making smarter software and business investment decisions. It ensures alignment between strategy, people, processes and technology while reducing risk, saving time, and improving outcomes. The ISG approach promotes data-driven decision-making and collaboration, helping choose the right software providers for maximum value and return on investment.

Process Intelligence Platforms Emerging Providers

Over the next 12 to 24 months, CIOs and business leaders will prioritize end-to-end process transparency, efficiency gains and risk reduction to unlock measurable productivity from prior digital investments. As hybrid application landscapes expand across ERP, CRM, SaaS and legacy systems, limited visibility into cross-functional workflows has become a constraint on margin, customer experience and compliance. Enterprises are consolidating siloed deployments of RPA, BPM and process mining tools, shifting from static documentation to continuous, data-driven monitoring and tying automation initiatives to KPI-backed value streams. Advances in machine learning, generative AI and agentic AI are accelerating discovery, conformance checking, root-cause analysis and recommendation generation, driving demand for platforms that ingest operational telemetry, surface actionable insights and coordinate targeted remediation.

ISG Research defines process intelligence platforms as a data-driven approach to process optimization and continuous improvement. Process intelligence begins with discovery and mining that analyze event logs and system data to reveal how processes operate, identify inefficiencies and recommend improvements. Once opportunities are prioritized against organizational KPIs, process intelligence coordinates with task automation and orchestration to implement effective automation workflows. By integrating with enterprise systems and accessing structured, semi-structured and unstructured data, process intelligence supports insights that improve operational performance, compliance and business outcomes.

ISG Research defines process intelligence platforms as a data-driven approach to process optimization and continuous improvement. Process intelligence begins with discovery and mining that analyze event logs and system data to reveal how processes operate, identify inefficiencies and recommend improvements. Once opportunities are prioritized against organizational KPIs, process intelligence coordinates with task automation and orchestration to implement effective automation workflows. By integrating with enterprise systems and accessing structured, semi-structured and unstructured data, process intelligence supports insights that improve operational performance, compliance and business outcomes.

ISG Research monitors a group of emerging process intelligence providers that address targeted use cases or specific market segments. These offerings may deliver strong value within defined scenarios, but often lack the end-to-end visibility, governance depth or enterprise-scale deployment required for inclusion in the main Buyers Guide. As a result, they are assessed separately as specialized or evolving options rather than full platform replacements.

Process intelligence platforms are industry-agnostic, but see the strongest adoption in high-volume and compliance-sensitive domains such as financial services, healthcare, manufacturing, telecom and the public sector. By 2027, 1 in 5 enterprises will adopt GenAI-powered process intelligence software to effectively describe and visualize business process automation, reinforcing demand for platforms that move beyond reporting to actionable insight. These platforms are best suited for large enterprises managing complex, cross-system processes such as order-to-cash, procure-to-pay, customer service and claims.

Successful adoption depends on broad connectivity to source systems and event logs, rigorous data normalization and lineage and clearly defined process ownership with KPI frameworks. Enterprises also require an operating model that can act on insights through RPA, workflow orchestration, intelligent document processing and integration tooling. Effective deployments typically begin with discovery and conformance analysis in a small set of high-impact processes, progress to simulation and what-if modeling, and then advance to closed-loop optimization that links insights directly to automated actions and outcome measurement. Mid-market organizations often favor SaaS delivery with prebuilt connectors, best-practice templates and low-overhead data pipelines to accelerate time-to-value and demonstrate ROI.

The category has evolved from traditional BPM and static documentation toward data-driven discovery and continuous monitoring. Early approaches relied on workshops and manual mapping, which proved inaccurate and slow across complex ERP, CRM and SaaS environments. The introduction of process mining enabled fact-based discovery through event-log analysis, providing objective views of how processes actually executed compared with designed flows.

Enterprises evaluating process intelligence require end-to-end transparency across value streams.

Recent advances in machine learning and generative AI have expanded process intelligence from diagnostics to optimization. Platforms now support root-cause analysis, bottleneck detection and scenario simulation, and increasingly connect insights to orchestration tools for execution. This evolution reflects enterprise demand to link process performance directly to KPIs for quality, throughput, cost and compliance, and to sustain continuous improvement rather than one-time reengineering efforts.

Enterprises evaluating process intelligence require end-to-end transparency across value streams. This starts with comprehensive ingestion of event logs and operational telemetry, strong data preparation and lineage and KPI frameworks that connect findings to margin, risk and customer experience. The ability to move from insight to action is critical, with identified inefficiencies triggering workflow changes, automation or policy updates instead of static reports.

Interoperability and responsible AI underpin scale. Organizations need clear governance policies, model lifecycle management and human-in-the-loop controls for risk-sensitive processes. Platforms must integrate through APIs and event streams with core systems and interoperate with orchestration and IDP tools to address execution and data quality. These capabilities enable measurable improvements in straight-through processing, cycle time and compliance without disrupting existing operations.

When evaluating emerging process intelligence platforms, enterprises should focus on how specialized capabilities align with specific processes, industries or analytic needs.

Effective process intelligence platforms deliver cohesive capabilities across discovery, mining, conformance checking and root-cause analysis, supported by simulation and what-if modeling to quantify impact. They ingest data from diverse enterprise sources, provide connectors and SDKs for integration and include data preparation features to ensure reliable insights. Embedded ML and GenAI should enhance anomaly detection, recommendation generation and narrative explanation under configurable guardrails.

Governance, security and actionability remain essential. Platforms should provide role-based access, audit trails, privacy controls for PII and PHI, data residency support and model monitoring for drift and bias. Analytics must translate into decisions through benchmarks, target-setting and impact tracking, with handoffs to RPA, workflow engines and IDP for execution. Runtime dashboards should track outcomes such as accuracy, throughput, rework and SLA adherence to validate ROI and sustain improvement.

When evaluating emerging process intelligence platforms, enterprises should focus on how specialized capabilities align with specific processes, industries or analytic needs. These offerings can deliver differentiated insight or innovation, but typically require integration with broader automation and orchestration platforms to meet enterprise requirements for governance, scale and closed-loop execution.

The 2026 ISG Buyers Guide™ for Process Intelligence Platforms Emerging Providers evaluates software providers across key capability areas, including process discovery and mining, conformance analysis, root-cause analysis, predictive and cognitive analytics, data ingestion and preparation, integration frameworks, visualization and modeling, automation handoffs and governance and security controls. This research assesses the following providers: Apromore, AuraQuantic, BusinessOptix, Fisent, Hubbl, ITyX, JobRouter, Mehrwerk, Mimica, mindzie, QPR Software, Skan AI and StereoLOGIC.

Key Takeaways

Enterprises are adopting process intelligence to gain objective visibility into how cross-system processes actually execute and where inefficiencies, risk and rework occur. The category has evolved from static BPM documentation toward continuous, data-driven discovery, conformance analysis and optimization grounded in operational telemetry. Emerging providers are addressing targeted use cases and segments with differentiated analytics, but often require integration with broader automation and orchestration stacks to support enterprise-scale governance and closed-loop execution.

Software Provider Summary

The ISG Buyers Guide™ for Process Intelligence Platforms Emerging Providers evaluates 13 software providers offering products that support process discovery, mining, conformance analysis and data-driven optimization across enterprise workflows. The research ranked the top three overall leaders as QPR Software, Apromore and Hubbl. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. Apromore, AuraQuantic, Hubbl, Mimica, QPR Software and Skan AI were rated as Exemplary, with Fisent rated as Innovative. BusinessOptix was rated as Assurance, and ITyX, JobRouter, Mehrwerk, Mindzie and StereoLOGIC were rated as Merit.

Product Experience Insights

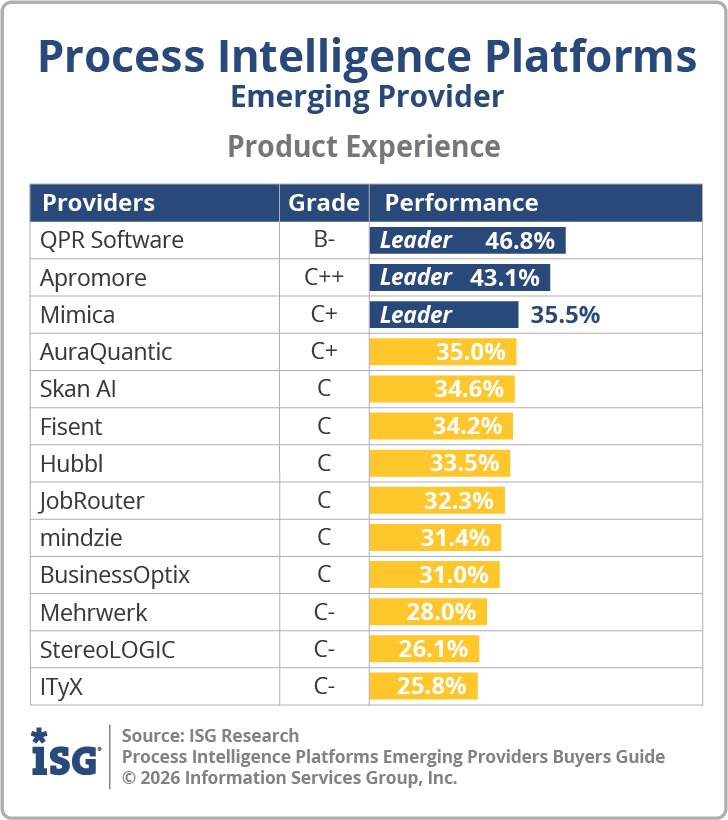

Product Experience, representing 80% of the evaluation, focuses on Capability (50%) and Platform (30%), which includes adaptability, manageability, reliability and usability. QPR Software, Apromore and Mimica achieved the highest performance as Leaders in this category, supported by breadth and depth in data-driven process discovery and mining, and enterprise-grade platform adaptability across complex ERP, CRM and SaaS environments. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

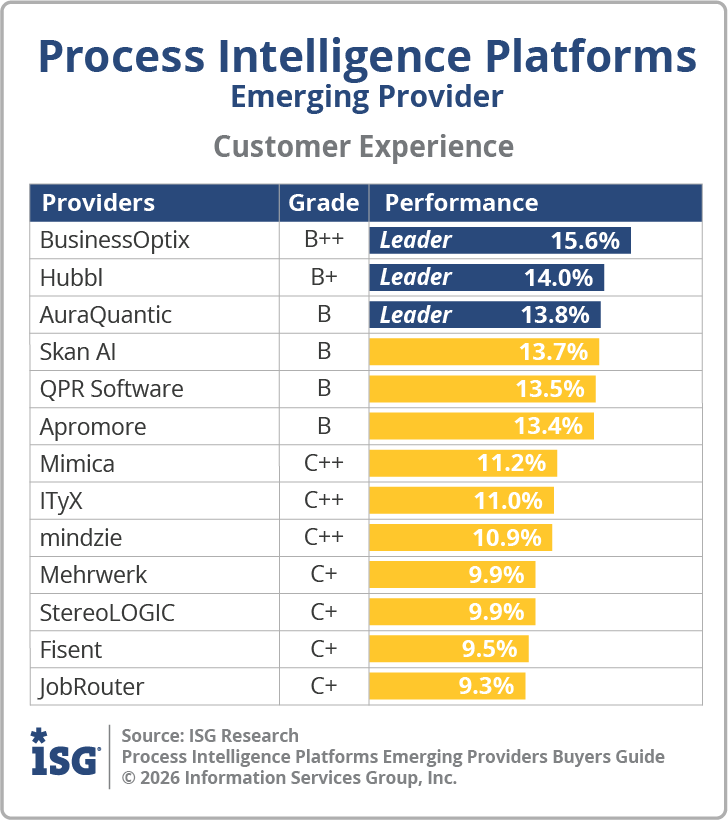

Customer Experience, representing 20% of the evaluation, focuses on validation and TCO/ROI. BusinessOptix, Hubbl and AuraQuantic were the Leaders in this category, showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should align emerging process intelligence platforms to specific processes, industries or analytic objectives rather than treating them as full platform replacements. Buyers should prioritize software that combines strong data ingestion and normalization with clear handoffs to automation, orchestration and integration tooling. Effective selection requires balancing specialized insight with governance readiness so insights can translate into measurable, KPI-linked outcomes.

The Findings – Process Intelligence Platforms Emerging Providers

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

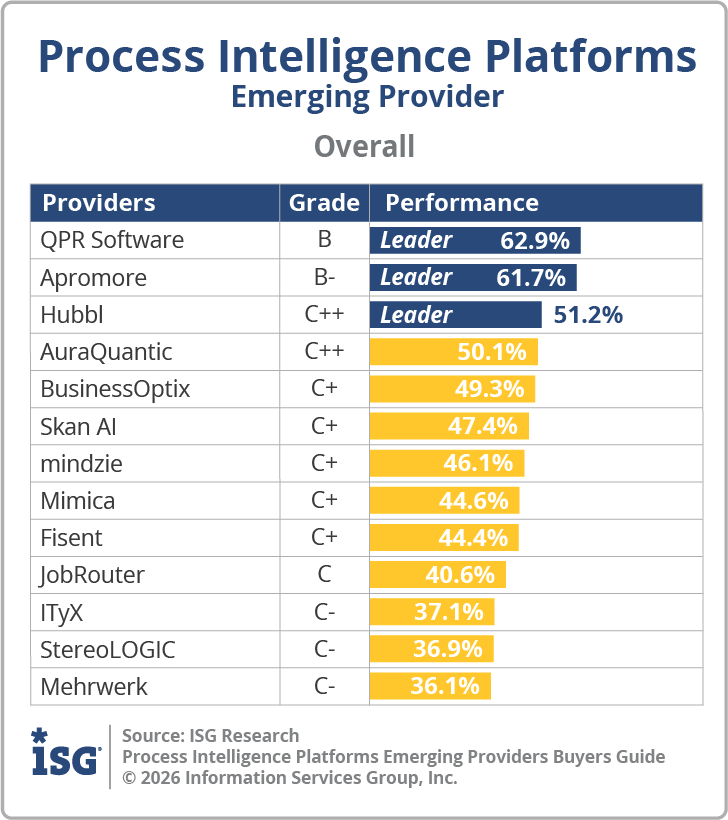

Overall Scoring of Software Providers Across Categories

The research finds QPR Software atop the list, followed by Apromore and Hubbl. Providers that place in the top three of a category earn the designation of Leader. QPR Software has done so in four categories, Apromore and Hubbl in three, Mimica in two and AuraQuantic, BusinessOptix and Skan AI in one category.

The research finds QPR Software atop the list, followed by Apromore and Hubbl. Providers that place in the top three of a category earn the designation of Leader. QPR Software has done so in four categories, Apromore and Hubbl in three, Mimica in two and AuraQuantic, BusinessOptix and Skan AI in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: Apromore, AuraQuantic, Hubbl, Mimica, QPR Software and Skan AI.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The provider rated Innovative is: Fisent.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The provider rated Assurance is: BusinessOptix.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: ITyX, JobRouter, Mehrwerk, mindzie and StereoLOGIC.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (50%) and Platform (30%). QPR Software, Apromore and Mimica were designated Product Experience Leaders. While not a Leader, AuraQuantic was also found to meet a broad range of enterprise product experience requirements.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are BusinessOptix, Hubbl and AuraQuantic. These category leaders best communicate commitment and dedication to customer needs. While not a Leader, Skan AI was also found to meet a broad range of enterprise customer experience requirements.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Process Intelligence Platforms Emerging Providers

For inclusion in the 2026 ISG Buyers Guide™ for Process Intelligence Platforms Emerging Providers, a software provider must be in good standing financially and ethically, have at least $1 million but not more than $20 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents and have at least 15 full-time employees. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer suites or packages of products that may include relevant individual modules or applications. If a software provider is actively marketing, selling and developing a product for the general market and it is reflected on the provider’s website that the product is within the scope of the research, that provider is automatically evaluated for inclusion.

All software providers that offer relevant products and meet the inclusion requirements were invited to participate in the evaluation process at no cost to them.

Software providers that meet our inclusion criteria but did not completely participate in our Buyers Guide were assessed solely on publicly available information. As this could have a significant impact on classification and ratings, we recommend additional scrutiny when evaluating those providers.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| AuraQuantic | Process mining and data | N/A | June 2025 |

| BusinessOptix | BusinessOptix | N/A | September 2025 |

| Fisent | Fisent BizAI | N/A | June 2025 |

| Hubbl | Hubbl Process Intelligence | 2.71 | October 2025 |

| ITyX | ITyX AI Platform | 2.10 | May 2024 |

| JobRouter | JobRouter | 2025.2 | September 2025 |

| Mehrwerk | mpmX Process Excellence Platform | 2.6 | July 2025 |

| Mimica | Mimica Miner | N/A | January 2025 |

| mindzie | mindzie Process Mining | 2.0 | August 2025 |

| QPR Software | QPR ProcessAnalyzer | 2025.7 | November 2025 |

| Salesforce | Apromore | 10.4 | September 2025 |

| Skan AI | Skan AI | N/A | October 2025 |

| StereoLOGIC | StereoLOGIC | N/A | September 2025 |

Intelligent Document Processing Platforms Emerging Providers

IDP platforms combine optical character recognition and computer vision, natural language processing and machine learning, augmented by generative and agentic AI.

Over the next 12 to 24 months, CIOs and IT leaders will prioritize converting unstructured content into actionable data to improve straight-through processing, compliance and customer experience across document-intensive workflows. The volume and variability of enterprise documents continue to grow, while talent constraints and regulatory scrutiny around privacy, data residency and auditability demand higher accuracy with stronger controls. Enterprises are consolidating legacy OCR tools into AI-enabled platforms, adopting foundation models with human-in-the-loop review for risk-sensitive processes and integrating document intelligence with process mining, orchestration and line-of-business systems to close the loop from insight to action. Advances in machine learning, generative AI and agentic AI are increasing extraction precision, enabling semantic understanding and automating validation and exception handling, driving demand for IDP platforms that deliver enterprise-grade accuracy, governance and interoperability.

ISG Research defines intelligent document processing platforms as enterprise software that automates the extraction, classification, analysis and processing of information from structured, semi-structured and unstructured documents. These platforms combine optical character recognition and computer vision, natural language processing and machine learning, augmented by generative and agentic AI, to understand, validate and act on document content. Core capabilities include multichannel ingestion; layout and semantic understanding; entity and table extraction; policy- and model-driven validation; human-in-the-loop review; enrichment and routing; integration with process intelligence, automation and orchestration systems; and analytics and quality monitoring, supported by security, privacy and access controls. The objective is to increase automation rates, reduce cycle times and errors and provide governed, auditable document intelligence at enterprise scale.

ISG Research also tracks a group of emerging IDP providers whose offerings apply AI to document-centric use cases but do not meet the inclusion requirements for the main Buyers Guide. These providers often focus on specific document types, industries or processing tasks, and may be earlier in platform maturity or enterprise adoption. While many demonstrate strong innovation in areas such as classification, extraction or language understanding, they typically lack the breadth of document coverage or enterprise deployment footprint associated with leading IDP platforms and are positioned as complementary alternatives.

IDP platforms are industry-agnostic but see the strongest adoption in document-heavy and compliance-sensitive domains such as financial services, insurance, healthcare, public sector, manufacturing and logistics and energy and utilities. By 2028, enterprise IT leaders will favor AI-driven document automation with built-in governance and validation to accelerate straight-through processing while preserving accuracy, compliance and trust at scale, reinforcing demand for platforms that move beyond point automation. These platforms are best suited for large enterprises managing high document volumes, variability and multilingual requirements across hybrid and multicloud environments.

IDP platforms are industry-agnostic but see the strongest adoption in document-heavy and compliance-sensitive domains such as financial services, insurance, healthcare, public sector, manufacturing and logistics and energy and utilities. By 2028, enterprise IT leaders will favor AI-driven document automation with built-in governance and validation to accelerate straight-through processing while preserving accuracy, compliance and trust at scale, reinforcing demand for platforms that move beyond point automation. These platforms are best suited for large enterprises managing high document volumes, variability and multilingual requirements across hybrid and multicloud environments.

Successful adoption depends on defined data governance and privacy policies for handling PII and PHI, representative training datasets and established human-in-the-loop quality assurance for exception management. Enterprises also require model lifecycle management that includes versioning, monitoring and drift detection, along with integration maturity through APIs and event streams connecting IDP to ERP, CRM, enterprise content management and workflow tools. Effective deployments typically begin with high-impact document flows such as invoice-to-pay, claims intake or customer onboarding, establish accuracy and straight-through processing targets and expand incrementally to more complex, multi-format content. Mid-market organizations often favor SaaS delivery with pre-trained models, template libraries and usage-based pricing to accelerate time-to-value while maintaining governance.

The category has evolved from template-driven OCR and rules-based classification toward AI-enabled document intelligence capable of handling high variability and scale. Early solutions digitized structured forms and invoices but struggled with unstructured content, multilingual inputs and complex layouts. Advances in computer vision, NLP and machine learning expanded extraction accuracy and coverage, while human-in-the-loop review improved reliability in compliance-sensitive workflows.

The infusion of generative and agentic AI has accelerated this evolution. Today’s IDP platforms now perform semantic understanding, contextual validation and narrative summarization, and integrate with process intelligence and orchestration systems. This shift moves IDP from point tools toward enterprise platforms that convert document content into governed data and trigger downstream actions, enabling measurable gains in straight-through processing under strong governance.

Enterprises evaluating IDP platforms require the ability to transform diverse documents into accurate, auditable data that supports end-to-end automation. This starts with multichannel ingestion, robust extraction of text, tables and entities and policy-based validation aligned to business rules and regulatory requirements. Embedded metrics for accuracy, straight-through processing and operational performance are needed to connect document processing improvements to cycle time reduction, error rates and customer experience.

Interoperability and responsible AI are equally important. IDP platforms must integrate through APIs and event streams with core business systems to route enriched data and manage exceptions. Governance must extend across data privacy, residency and model operations, supported by human-in-the-loop checkpoints for workflows carrying regulatory or financial risk. These foundations enable organizations to expand confidently from structured documents to complex, unstructured content.

Effective IDP platforms deliver cohesive, native capabilities across OCR and computer vision, NLP and machine learning for layout and semantic understanding and flexible validation that combines rules, models and referential data. Platforms should provide annotation tools to accelerate model improvement, human-in-the-loop review and enrichment and routing to downstream systems. Generative AI should augment classification, summarization and exception guidance under configurable guardrails.

Emerging offerings can deliver differentiated innovation but typically require integration with broader platforms to meet enterprise needs for scale, governance and closed-loop execution.

Scale and governance remain non-negotiable. Platforms must provide role-based access control, audit trails, secrets management and compliance attestations, along with multilingual support and connectors or SDKs for integration. Model operations, including dataset quality management, evaluation pipelines, bias checks and continuous monitoring, should be built in, supported by reliability features and deployment flexibility across SaaS and hybrid environments with cost transparency.

When assessing emerging IDP providers, enterprises should focus on how specialized capabilities align with specific document types, industries or processing requirements. These offerings can deliver differentiated innovation, but typically require integration with broader process intelligence, automation and orchestration platforms to meet enterprise needs for scale, governance and closed-loop execution.

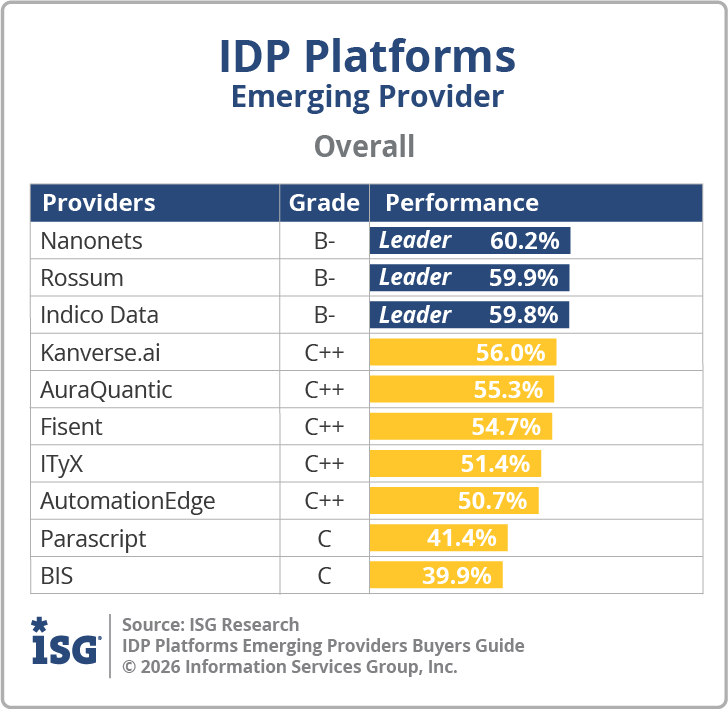

The 2026 ISG Buyers Guide™ for Intelligent Document Processing Platforms Emerging Providers evaluates software providers across key capability areas, including data extraction and recognition, document classification and categorization, AI and machine learning functionality, integration and export, error reduction and validation, model scalability and adaptability and support for no-code, low-code and pro-code interfaces. This research assesses the following providers: AuraQuantic, AutomationEdge, BIS, Fisent, Indico Data, ITyX, Kanverse.ai, Nanonets, Parascript and Rossum.

Key Takeaways

Enterprises are accelerating adoption of intelligent document processing to convert growing volumes of unstructured content into governed, auditable data that improves straight-through processing, compliance and customer experience. The category has progressed from template-driven OCR and rules-based classification to AI-enabled semantic understanding, human-in-the-loop validation and integrated model lifecycle controls that enable higher accuracy at scale. Emerging providers deliver differentiated capabilities for specific document types or industries, but generally require integration with process intelligence, orchestration and broader automation stacks to achieve enterprise governance and closed-loop execution.

Software Provider Summary

The ISG Buyers Guide™ for Intelligent Document Processing Platforms Emerging Providers evaluates 10 software providers offering products that support document ingestion, classification, extraction, validation and export across document-intensive enterprise workflows. The research ranked the top three overall leaders as Nanonets, Rossum and Indico Data. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. AuraQuantic, Indico Data and Nanonets were rated as Exemplary, with Fisent and Rossum rated as Innovative. AutomationEdge and Kanverse.ai were rated as Assurance, and BIS, ITyX and Parascript were rated as Merit.

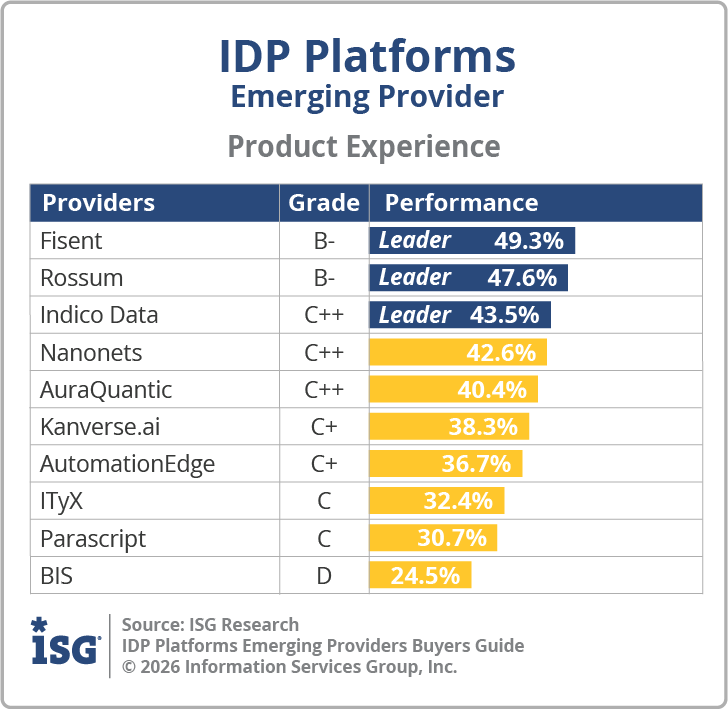

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (50%) and Platform (30%), which includes adaptability, manageability, reliability and usability. Fisent, Rossum and Indico Data achieved the highest performance as Leaders in this category, supported by advanced extraction and layout/semantic understanding and robust model operations and governance. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

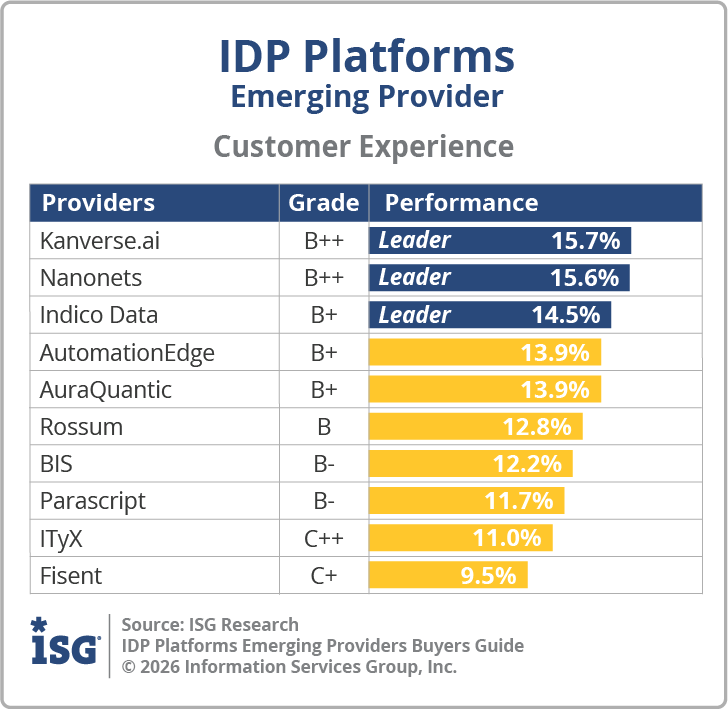

Customer Experience, representing 20% of the evaluation, focuses on validation and TCO/ROI. Kanverse.ai, Nanonets and Indico Data were the Leaders in this category, showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Prioritize IDP pilots on high-impact, document-heavy flows (for example, invoice-to-pay, claims intake or onboarding) with clear straight-through processing and accuracy targets, and expand incrementally after establishing governance and model-ops controls. Require multichannel ingestion, policy-driven validation and human-in-the-loop checkpoints for risk-sensitive use cases, and demand connectors or event streams that enable closed-loop handoffs to process intelligence, orchestration and downstream systems. Evaluate providers for built-in model lifecycle management, audit trails and role-based access to ensure regulatory and privacy requirements are met while maintaining operational scale.

The Findings – Intelligent Document Processing Platforms Emerging Providers

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

Overall Scoring of Software Providers Across Categories

The research finds Nanonets atop the list, followed by Rossum and Indico Data. Providers that place in the top three of a category earn the designation of Leader. Indico Data has done so in five categories, Nanonets and Rossum in three, Fisent in two and ITyX and Kanverse.ai in one category.

The research finds Nanonets atop the list, followed by Rossum and Indico Data. Providers that place in the top three of a category earn the designation of Leader. Indico Data has done so in five categories, Nanonets and Rossum in three, Fisent in two and ITyX and Kanverse.ai in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: AuraQuantic, Indico Data and Nanonets.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The providers rated Innovative are: Fisent and Rossum.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The providers rated Assurance are: AutomationEdge and Kanverse.ai.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: BIS, ITyX and Parascript.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (50%) and Platform (30%). Fisent, Rossum and Indico Data were designated Product Experience Leaders.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are Kanverse.ai, Nanonets and Indico Data. These category leaders best communicate commitment and dedication to customer needs.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Intelligent Document Processing Platforms Emerging Providers

For inclusion in the 2026 ISG Buyers Guide™ for Intelligent Document Processing Platforms Emerging Providers, a software provider must be in good standing financially and ethically, have at least $2.5 million but no more than $45 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents and have at least 15 full-time employees. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer suites or packages of products that may include relevant individual modules or applications. If a software provider is actively marketing, selling and developing a product for the general market and it is reflected on the provider’s website that the product is within the scope of the research, that provider is automatically evaluated for inclusion.

All software providers that offer relevant products and meet the inclusion requirements were invited to participate in the evaluation process at no cost to them.

Software providers that meet our inclusion criteria but did not completely participate in our Buyers Guide were assessed solely on publicly available information. As this could have a significant impact on classification and ratings, we recommend additional scrutiny when evaluating those providers.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| AuraQuantic | AuraQuantic IDP | N/A | June 2025 |

| AutomationEdge | DocEdge | 8.2.1 | December 2025 |

| BIS | Grooper | N/A | June 2025 |

| Fisent | Fisent BizAI | N/A | June 2025 |

| Indico Data | Intelligent intake software | 7.5 | September 2025 |

| ITyX | Intelligent Document Processing (IDP) | 2.10 | May 2024 |

| Kanverse.ai | Kanverse Agentic Automation for Enterprises | Topaz | NA |

| Nanonets | Invoice OCR | Nanonets-OCR2 | October 2025 |

| Parascript | Parascript Intelligent Document Processing | PRS | September 2025 |

| Rossum | Intelligent Document Processing | N/A | August 2025 |

Automation and Orchestration Platforms Emerging Providers

Over the next 12 to 24 months, CIOs and IT leaders will intensify efforts to automate high-volume, rules-based tasks and orchestrate end-to-end workflows to improve productivity, reduce operational risk and capture measurable savings from prior digital investments. Rising labor costs, persistent talent shortages and fragmented application landscapes across ERP, CRM and SaaS environments are accelerating a shift from isolated RPA scripts toward enterprise-wide automation fabrics. Enterprises are consolidating legacy bot estates, pairing task automation with process intelligence and embedding generative and agentic AI to handle variability and accelerate exception resolution. Organizations are also standardizing governance, expanding orchestration beyond desktop automation to API- and event-driven integration and measuring outcomes against business KPIs, driving demand for platforms that combine reliability, security and AI-enabled flexibility as native capabilities.

Emerging providers are often earlier in maturity or focused on specific automation domains, workflow types or operational functions.

ISG Research defines automation and orchestration platforms as software platforms that automate repetitive, rule-based tasks across applications and systems and coordinate workflows across the enterprise. Originally centered on robotic process automation that emulated human actions for high-volume transactional work, these platforms now integrate RPA and generative AI to support task automation, process automation and orchestration. By integrating with enterprise systems and accessing structured, semi-structured and unstructured data, automation and orchestration platforms enable operational insight and continuous improvement without reliance on external managed services.

ISG Research also tracks emerging automation and orchestration providers whose offerings intersect this market but do not meet the inclusion criteria for the main Buyers Guide. These providers are often earlier in maturity or focused on specific automation domains, workflow types or operational functions. While many demonstrate innovation within defined use cases, they typically lack the orchestration breadth, enterprise deployment scale or integration depth required of comprehensive automation and orchestration platforms and are assessed separately as complementary or developing alternatives.

Automation and orchestration platforms support attended and unattended automation, UI- and API-level integration, event-driven triggers, human-in-the-loop exception handling and centralized orchestration that coordinates bots, AI agents and workflow engines across distributed environments. By 2027, over 70% of enterprises will standardize on a single digital platform for workflow automation and will deploy intelligent automation technologies to eliminate redundant manual work, reinforcing the need for platforms that unify execution,  governance and insight.

governance and insight.

Adoption is industry-agnostic but particularly strong in transaction- and compliance-intensive sectors such as financial services, insurance, healthcare, public sector, manufacturing, logistics, telecom and retail. These platforms are best suited for large enterprises with significant volumes of repeatable tasks across multiple systems and an operating model supported by an automation center of excellence or platform engineering function. Prerequisites for success include process discovery tied to business KPIs, integration maturity that extends beyond UI automation to APIs and event streams, robust change management and testing practices and clear policies for responsible AI use and data privacy.

Effective deployments typically begin with well-defined, rules-based tasks to capture early value, then expand to end-to-end workflows that integrate intelligent document processing, process intelligence and core business systems. As maturity increases, organizations introduce generative and agent-driven capabilities under strong guardrails. Mid-market organizations often favor SaaS delivery with prebuilt templates, opinionated best practices and transparent pricing to accelerate time-to-value while maintaining governance and measurable outcomes.

The category has evolved from early RPA tools that emulated human actions on user interfaces to enterprise automation fabrics that coordinate tasks across APIs, events and workflows. Initial deployments delivered quick wins but struggled with variability, exception handling and brittle integrations. As application landscapes expanded across ERP, CRM, SaaS and custom services, orchestration became essential to support scale, parallel processing and auditability.

Advances in machine learning, generative AI and event-driven architectures have accelerated this evolution. Today’s platforms blend attended and unattended automation with API-first integration, incorporate human-in-the-loop oversight where risk requires it and connect with process intelligence and intelligent document processing. The emphasis has shifted from isolated bots to closed-loop execution models, where insights identify improvement opportunities, orchestration implements changes under policy guardrails and analytics validate outcomes against KPIs.

Enterprises require end-to-end automation that increases straight-through processing, reduces cycle times and improves customer and employee experience. This begins with a holistic view of value streams, such as order-to-cash, procure-to-pay, claims and onboarding, supported by KPIs that prioritize use cases and measure impact. Automation must convert unstructured content into governed data, route tasks reliably across systems and surface exceptions for timely resolution.

Effective platforms deliver cohesive capabilities across design, execution and governance.

Scale depends on interoperability and responsible AI. Platforms must provide broad connectivity through APIs, event streams and connectors, standardize identity, access and audit controls and enforce privacy and data residency requirements. AI adoption requires explicit usage policies, model lifecycle management and human-in-the-loop checkpoints for risk-sensitive steps. Operating models that pair an automation center of excellence with platform engineering are critical to codifying patterns, managing change and ensuring reuse.

Effective automation and orchestration platforms deliver cohesive capabilities across design, execution and governance. Core functions include low-code development, connector libraries, UI-, API- and event-driven automation, queueing and scheduling, versioning and change control and run-time monitoring and analytics that quantify throughput, accuracy, rework and compliance. AI should enhance these capabilities through document understanding, classification, contextual guidance and supervised exception handling under configurable guardrails.

Enterprise-grade governance and resilience are non-negotiable. Platforms must provide role-based access control, Policy-as-Code, secrets management, audit trails and compliance attestations, along with fault tolerance, retries and rollback. Integration with intelligent document processing, process intelligence and core business systems is essential, supported by deployment flexibility and cost transparency as automation scales.

When evaluating emerging automation and orchestration providers, enterprises should assess how focused capabilities align with specific processes or operational gaps. These offerings can deliver differentiated innovation but typically require integration with broader platforms to meet enterprise requirements for governance, scale and closed-loop execution.

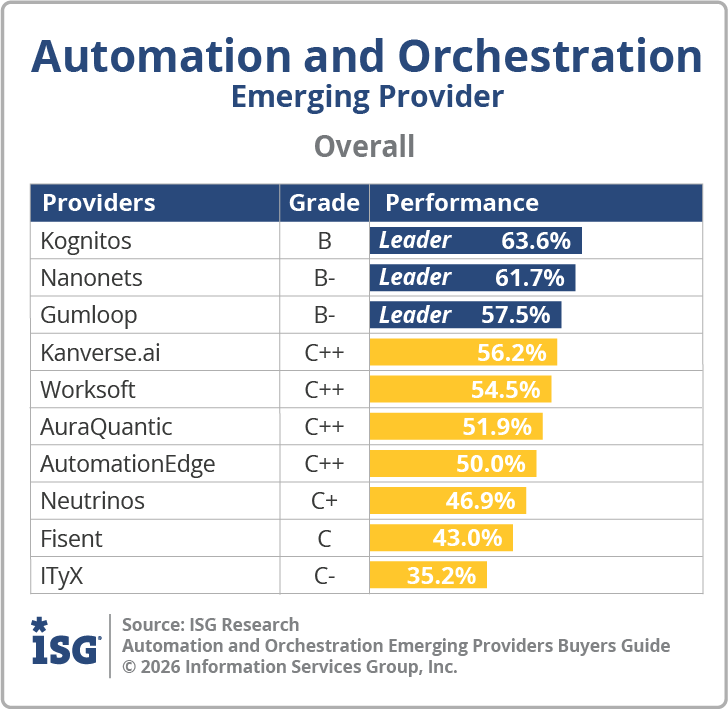

The 2026 ISG Buyers Guide™ for Automation and Orchestration Platforms Emerging Providers evaluates software providers across key capability areas, including attended and unattended automation, system integration, natural language processing, data analytics, workflow design, user interface innovation, AI and machine learning support, cognitive automation, error handling, exception management and orchestration functionality. This research assesses the following providers: AuraQuantic, AutomationEdge, Fisent, Gumloop, ITyX, Kanverse.ai, Kognitos, Nanonets, Neutrinos and Worksoft.

Key Takeaways

Automation and orchestration platforms are evolving from isolated RPA deployments into enterprise automation fabrics that coordinate tasks, workflows and AI-driven actions across systems. Growing application sprawl, labor constraints and governance requirements are pushing enterprises to consolidate bots, standardize orchestration and tie automation outcomes directly to business KPIs. Emerging providers address focused automation scenarios with innovation, but typically require integration with broader platforms to support enterprise-scale governance, interoperability and closed-loop execution.

Software Provider Summary

The ISG Buyers Guide™ for Automation and Orchestration Platforms Emerging Providers evaluates 10 software providers offering products supporting task automation, workflow orchestration and enterprise integration. The research ranked the top three overall leaders as Kognitos, Nanonets and Gumloop. Providers were classified using weighted performance in Product Experience and Customer Experience for ISG quadrant placement. Kanverse.ai, Kognitos and Nanonets were rated as Exemplary, with Gumloop and Worksoft rated as Innovative. AuraQuantic and AutomationEdge were rated as Assurance, and Fisent, ITyX and Neutrinos were rated as Merit.

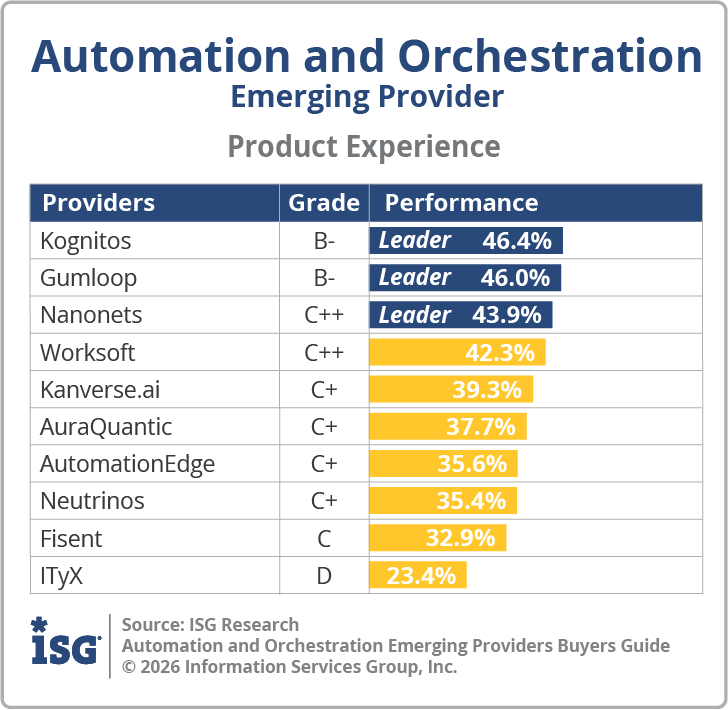

Product Experience Insights

Product Experience, representing 80% of the evaluation, focuses on Capability (40%) and Platform (40%), which includes adaptability, manageability, reliability and usability. Kognitos, Gumloop and Nanonets achieved the highest performance as Leaders in this category, supported by breadth in automation and orchestration capabilities and strong platform foundations for API-, event- and UI-driven execution. Leaders demonstrated enterprise-grade platform capabilities across varied roles and contexts.

Customer Experience Value

Customer Experience, representing 20% of the evaluation, focuses on validation and TCO/ROI. Kanverse.ai, Kognitos and Nanonets were the Leaders in this category, showing strong customer advocacy and clear investment in success outcomes. Providers with lower performance often lacked publicly available customer validation or failed to demonstrate structured ROI measurement and proactive lifecycle engagement.

Strategic Recommendations

Enterprises should anchor automation initiatives in prioritized value streams with KPI-backed use cases rather than expanding isolated bots. Buyers should favor platforms that combine orchestration breadth, strong governance and responsible AI controls with integration beyond UI automation. Ensuring interoperability with process intelligence, IDP and core systems is essential to sustain scale and measurable outcomes.

The Findings – Automation and Orchestration Platforms Emerging Providers

The software providers and products evaluated in the research provide product and customer experiences, but not everything offered is equally valuable to every enterprise or is needed to operate in business processes and use cases. Moreover, the existence of too many capabilities in products may be a negative factor for an enterprise if it introduces unnecessary complexity. Nonetheless, you may decide that a more comprehensive set of capabilities in the product is important, and where they match your enterprise’s requirements.

An effective customer relationship with a software provider is vital to the success of any investment. The overall customer experience and the full lifecycle of engagement play a key role in ensuring satisfaction and long-term success. Providers with dedicated customer leadership, such as chief customer officers, tend to invest more deeply in these relationships and prioritize customer outcomes to TCO and ROI expectations. It is equally important that this commitment to customer success is clearly demonstrated throughout the provider’s website, buying process and customer journey.

Overall Scoring of Software Providers Across Categories

The research finds Kognitos atop the list, followed by Nanonets and Gumloop. Providers that place in the top three of a category earn the designation of Leader. Kognitos has done so in five categories, Gumloop and Nanonets in four and Neutrinos and Kanverse.ai in one category.

The research finds Kognitos atop the list, followed by Nanonets and Gumloop. Providers that place in the top three of a category earn the designation of Leader. Kognitos has done so in five categories, Gumloop and Nanonets in four and Neutrinos and Kanverse.ai in one category.

The overall representation of the research below places the rating of the Product Experience and Customer Experience on the x and y axes, respectively, to provide a visual representation and classification of the software providers. Those providers whose Product Experience have above median weighted performance to the axis in aggregate of the two product categories place farther to the right, while the performance and weighting for the Customer Experience category determines placement on the vertical axis. In short, software providers that place closer to the upper-right on this chart performed better than those closer to the lower-left.

The research categorizes and rates software providers into one of four categories: Assurance, Exemplary, Merit or Innovative. This representation of software providers’ weighted performance in meeting the requirements in product and customer experience.

Exemplary: This rating (upper right) represents those that performed above median in Product and Customer Experience requirements. The providers rated Exemplary are: Kanverse.ai, Kognitos and Nanonets.

Innovative: This rating (lower right) represents those that performed above median in Product Experience but not in Customer Experience. The providers rated Innovative are: Gumloop and Worksoft.

Assurance: This rating (upper left) represents those that performed above median in Customer Experience but not in Product Experience. The providers rated Assurance are: AuraQuantic and AutomationEdge.

Merit: This rating (lower left) represents those that did not surpass the median in Customer or Product Experience. The providers rated Merit are: Fisent, ITyX and Neutrinos.

We advise enterprises to use this research as a supplement to their own evaluations, recognizing that ratings or rankings do not solely represent the value of a provider nor indicate universal suitability of a set of products.

Product Experience

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The process of researching products to address an enterprise’s needs should be comprehensive and evaluate specific capabilities and the underlying platform to the product experience. Our evaluation of the Product Experience examines the lifecycle of onboarding, configuration, operations, usage and maintenance. Too often, software providers are not evaluated for the entirety of the product; instead, they are evaluated on market execution and vision of the future.

The research results in Product Experience are ranked at 80%, or four-fifths, using the underlying weighted performance. Importance was placed on the categories as follows: Capability (40%) and Platform (40%). Kognitos, Gumloop and Nanonets were designated Product Experience Leaders.

Customer Experience

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The importance of a customer relationship with a software provider is essential to the actual success of the products and technology. The evaluation of the Customer Experience and the entire lifecycle an enterprise has with its software provider is critical for ensuring satisfaction in working with that provider. The ISG Buyers Guide examines a software provider’s customer commitment, viability, customer success, sales and onboarding, product roadmap and services with partners and support. The customer experience category also investigates the TCO/ROI and how well a software provider demonstrates the product’s overall value, cost and benefits, including the tools and resources to evaluate these factors.

The research results in Customer Experience are ranked at 20%, or one-fifth of the 100% index, and represent the underlying provider validation and TCO/ROI requirements as they relate to the framework of commitment and value to the software provider-customer relationship.

The software providers that evaluated the highest in the Customer Experience category are Kanverse.ai, Kognitos and Nanonets. These category leaders best communicate commitment and dedication to customer needs.

Software providers that did not perform well in this category were unable to provide or make sufficient information readily available to demonstrate success or articulate their commitment to customer experience. The use of a software provider requires continuous investment, so a holistic evaluation must include examination of how they support their customer experience.

Software Provider Inclusion – Automation and Orchestration Platforms Emerging Providers

For inclusion in the 2026 ISG Buyers Guide™ for Automation and Orchestration Platforms Emerging Providers, a software provider must be in good standing financially and ethically, have at least $400,000 but not more than $32 million in annual or projected revenue verified using independent sources, sell products and provide support on at least two continents. The principal source of the relevant business unit’s revenue must be software-related, and there must have been at least one major software release in the past 12 months.

The research is designed to be independent of the specifics of software provider packaging and pricing. To represent the real-world environment in which businesses operate, we include providers that offer suites or packages of products that may include relevant individual modules or applications. If a software provider is actively marketing, selling and developing a product for the general market and it is reflected on the provider’s website that the product is within the scope of the research, that provider is automatically evaluated for inclusion.

All software providers that offer relevant products and meet the inclusion requirements were invited to participate in the evaluation process at no cost to them.

Software providers that meet our inclusion criteria but did not completely participate in our Buyers Guide were assessed solely on publicly available information. As this could have a significant impact on classification and ratings, we recommend additional scrutiny when evaluating those providers.

Products Evaluated

| Provider | Product Names | Version | Release Month/Year |

|---|---|---|---|

| AuraQuantic | Business Process Automation | N/A | June 2025 |

| AutomationEdge | AutomationEdge | 8.2.1 | December 2025 |

| Fisent | Fisent BizAI | N/A | June 2025 |

| Gumloop | Gumloop | 6.2.0 | November 2025 |

| ITyX | Intelligent Document Processing (IDP) | 2.10 | May 2024 |

| Kanverse.ai | Kanverse Agentic Automation for Enterprises | Topaz | November 2025 |

| Kognitos | Kognitos Automation Intelligence Platform | main-c37cb91f95-43083 | October 2025 |

| Nanonets | Nanonets Workflow Automation | N/A | March 2025 |

| Neutrinos | Neutrinos Low-code Platform | 25.10-17.0.00 | October 2025 |

| Worksoft | Worksoft Connective Automation | 14.5 | June 2025 |

Executive Summary

Buyers Guide Overview

ISG Research has conducted market research for over two decades across vertical industries, business applications, AI and IT. We have designed the ISG Buyers Guide™ to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements. Utilization of our research methodology and decades of experience enables our Buyers Guide to be an effective method to assess and select software providers and products. The findings of this research provide a comprehensive approach to rating software providers and rank their ability to meet specific product and customer experience requirements.

ISG Research has designed the Buyers Guide to provide a balanced perspective of software providers and products that is rooted in an understanding of business and IT requirements.

The 2026 ISG Buyers Guides™ for Intelligent Automation Platforms Emerging Providers, covering Process Intelligence Platforms Emerging Providers, Intelligent Document Processing Platforms Emerging Providers and Automation and Orchestration Platforms Emerging Providers, are the distillation of continuous market and product research. It is an assessment of how well software providers’ offerings address enterprises’ requirements for intelligent automation software. The Value Index methodology is structured to support a request for information (RFI) for a request for proposal (RFP) process by incorporating all criteria needed to evaluate, select, utilize and maintain relationships with software providers. The ISG Buyers Guide evaluates customer experience and the product experience in its capability and platform.

The structure of the research reflects our understanding that the effective evaluation of software providers and products involves far more than just examining product features, potential revenue or customers generated from a provider’s marketing and sales efforts. It can ensure the best long-term relationship and value achieved from a resource and financial investment We believe it is important to take a comprehensive, research-based approach, since making the wrong choice of intelligent automation platform software can raise the total cost of ownership, lower the return on investment and hamper an enterprise’s ability to reach its potential. In addition, this approach can reduce the project’s development and deployment time and eliminate the risk of relying on opinions or historical biases.

ISG Research believes that an objective review of existing and potential new software providers and products is a critical strategy for the adoption and implementation of intelligent automation software. An enterprise’s review should include an analysis of both what is possible and what is relevant. We urge enterprises to do a thorough job of evaluating intelligent automation platforms and offer these Buyers Guides as both the results of our in-depth analysis of these providers and as an evaluation methodology.

How To Use This Buyers Guide

Evaluating Software Providers: The Process

We recommend using the Buyers Guide to assess and evaluate new or existing software providers for your enterprise. The market research can be used as an evaluation framework to assess existing approaches and software providers or establish a formal request for information from providers on products and customer experience and will shorten the cycle time when creating an RFI. The steps listed below provide a process that can facilitate best possible outcomes in the most efficient manner.

- Define the business case and goals.

Define the mission and business case for investment and the expected outcomes from your organizational and technological efforts. - Specify the business and IT needs.

Defining the business and IT requirements helps identify what specific capabilities are required with respect to people, processes, information and technology. - Assess the required roles and responsibilities.

Identify the individuals required for success at every level of the enterprise from executives to frontline workers and determine the needs of each. - Outline the project’s critical path.

What needs to be done, in what order and who will do it? This outline should make clear the prior dependencies at each step of the project plan. - Ascertain the technology approach.

Determine the business and technology approach that most closely aligns to your enterprise’s requirements. - Establish software provider evaluation criteria.

Utilize the product experience: capability and platform with support for adaptability, manageability, reliability and usability, and the customer experience in TCO/ROI and Validation. - Evaluate and select the software provider and products properly.

Apply a weighting the evaluation categories in the evaluation criteria to reflect your enterprise’s priorities to determine the short list of software providers and products. - Establish the business initiative team to start the project.

Identify who will lead the project and the members of the team needed to plan and execute it with timelines, priorities and resources.

Using the ISG Buyers Guide and process provides enterprises a clear, structured approach to making smarter software and business investment decisions. It ensures alignment between strategy, people, processes and technology while reducing risk, saving time, and improving outcomes. The ISG approach promotes data-driven decision-making and collaboration, helping choose the right software providers for maximum value and return on investment.

Process Intelligence Platforms Emerging Providers

Over the next 12 to 24 months, CIOs and business leaders will prioritize end-to-end process transparency, efficiency gains and risk reduction to unlock measurable productivity from prior digital investments. As hybrid application landscapes expand across ERP, CRM, SaaS and legacy systems, limited visibility into cross-functional workflows has become a constraint on margin, customer experience and compliance. Enterprises are consolidating siloed deployments of RPA, BPM and process mining tools, shifting from static documentation to continuous, data-driven monitoring and tying automation initiatives to KPI-backed value streams. Advances in machine learning, generative AI and agentic AI are accelerating discovery, conformance checking, root-cause analysis and recommendation generation, driving demand for platforms that ingest operational telemetry, surface actionable insights and coordinate targeted remediation.

ISG Research defines process intelligence platforms as a data-driven approach to process optimization and continuous improvement. Process intelligence begins with discovery and mining that analyze event logs and system data to reveal how processes operate, identify inefficiencies and recommend improvements. Once opportunities are prioritized against organizational KPIs, process intelligence coordinates with task automation and orchestration to implement effective automation workflows. By integrating with enterprise systems and accessing structured, semi-structured and unstructured data, process intelligence supports insights that improve operational performance, compliance and business outcomes.

ISG Research monitors a group of emerging process intelligence providers that address targeted use cases or specific market segments. These offerings may deliver strong value within defined scenarios, but often lack the end-to-end visibility, governance depth or enterprise-scale deployment required for inclusion in the main Buyers Guide. As a result, they are assessed separately as specialized or evolving options rather than full platform replacements.