Play audio

Instilling Confidence in the Era of Pillar Two and Beyond

Multinational Corporations Challenged by New Tax Rules

The Base Erosion and Profit Shifting (BEPS) initiative undertaken by the Organization for Economic Co-operation and Development (OECD) was designed to rein in what has been viewed as excessive tax avoidance by multinational corporations (MNCs). Crucially, the OECD does not have legal authority in this matter but provides recommendations to national governments on how to structure tax codes to address profit shifting by restricting tax avoidance and making international tax rates more equitable. When these recommendations are not universally adopted, it creates statutory patchworks that introduces additional complexity, risk and workloads in corporate tax departments.

ISG Research strongly recommends that tax departments have a third-party dedicated application or platform designed to meet the tax reporting and transparency requirements of MNCs.

Pillar Two establishes a global minimum tax framework through a set of interlocking rules. This structure not only complicates the mechanics of tax determination and provision, it also introduces the need for analysis to determine the best ways to allocate revenue and expenses wherever possible. Moreover, forecasting and analysis are necessary to take taxes into account when making decisions about transfer prices, siting operations, allocating production, choosing investments and determining capital structures as well as all mergers and acquisitions. Yet, as of this writing, Pillar Two will not be adopted by the United States, further complicating matters for tax departments and increasing the value of software to minimize workloads while providing deeper insight into how best to structure tax compliance.

ISG Research strongly recommends that tax departments have a third-party dedicated application or platform designed to meet the tax reporting and transparency requirements of MNCs with the flexibility to provide the specific analysis and reporting capabilities needed by individual organizations. Such a platform incorporates tax-specific logic and enables the department to plan and manage transfer pricing and tax reporting, as well as the specific requirements of Country-by-Country Reporting (CbCR), Pillar Two and any other subsequent tax legislation that introduces higher levels of complexity and scrutiny. A platform also allows the department to easily and consistently manage the data from across the entire enterprise working from a single source of truth. This helps reduce risks caused by data, formula or calculation errors, this provides more time for analysis and contingency planning to optimize tax payments, and it also helps boost the overall efficiency of the department.

Impact of Pillar Two-Type Changes on Tax Department Workloads

Pillar Two has already been adopted in part or in full by all the European Union members, the United Kingdom, Canada, Japan, South Korea and Australia. It has added a further level of complexity to tax calculations, analysis and compliance, increasing tax department workloads such that standalone spreadsheets are no longer an appropriate choice. To ensure compliance while reducing risk, corporate tax departments must be able to: collect and maintain all relevant data, which extends beyond that collected by financial management to include operational and human resources systems; utilize analytical tools to accurately optimize tax expense at the group, jurisdiction and local-entity level while respecting the parent’s risk parameters; and rapidly adjust corporate tax optimization plans and strategies as they update business forecasts country by country, or even at a legal-entity level, to achieve key performance objectives and financial metrics.

departments must be able to: collect and maintain all relevant data, which extends beyond that collected by financial management to include operational and human resources systems; utilize analytical tools to accurately optimize tax expense at the group, jurisdiction and local-entity level while respecting the parent’s risk parameters; and rapidly adjust corporate tax optimization plans and strategies as they update business forecasts country by country, or even at a legal-entity level, to achieve key performance objectives and financial metrics.

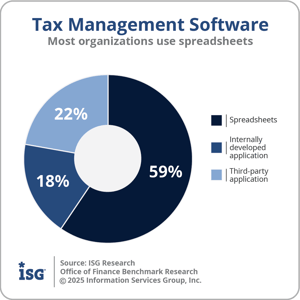

Unfortunately, our research found that 59% of organizations with 1,000 or more employees use spreadsheets to manage their taxes. Although spreadsheets are indispensable for many tasks, this manual approach cannot scale to handle the increasing data volumes as the number and complexity of calculations currently in place are exacerbated by Pillar Two. Tax departments must have a dedicated tax data and analytics platform to perform these essential functions. ISG Research advises organizations to find and deploy an alternative to spreadsheets immediately because departments need time to develop best practices for their corporation and translate these into processes that support these practices at the local, regional and headquarters levels.

The Global Tax Management Platform

A key capability of a global tax management platform is automatically gathering all necessary data for tax preparation, compliance, analysis and reporting directly from all systems of record, while enriching and transforming the data where necessary to ensure consistency in ways that satisfy the needs of the department.

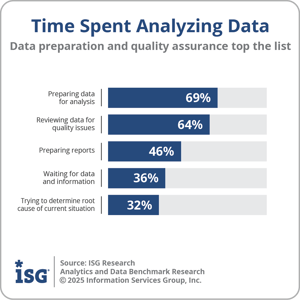

Today, manually assembling data consumes a significant amount of time for departments, along with checking and reconciling amounts to ensure accuracy. A platform that automates these processes substantially reduces the risk of errors in data and calculations that may be missed even with careful diligence, especially when facing tight deadlines. This is especially challenging when managing multiple tabs in multiple workbooks with different versions, handled by headquarters and local tax professionals. Our Analytics and Data Benchmark Research finds that 69% of organizations say preparing data is one of the most time-consuming aspects of analyzing data along with 64% that say reviewing data for quality and consistency is also an issue. Pillar Two amplifies the department’s data challenges since it requires that teams collect numbers and information from a broader range of sources, ensures that the data is assembled in a consistent fashion and records the data lineage for audit purposes. And all these additional layers of requirements need to be addressed and satisfied within existing time limits.

diligence, especially when facing tight deadlines. This is especially challenging when managing multiple tabs in multiple workbooks with different versions, handled by headquarters and local tax professionals. Our Analytics and Data Benchmark Research finds that 69% of organizations say preparing data is one of the most time-consuming aspects of analyzing data along with 64% that say reviewing data for quality and consistency is also an issue. Pillar Two amplifies the department’s data challenges since it requires that teams collect numbers and information from a broader range of sources, ensures that the data is assembled in a consistent fashion and records the data lineage for audit purposes. And all these additional layers of requirements need to be addressed and satisfied within existing time limits.

A dedicated tax platform retains all the information in an as-was state to facilitate audit defense, especially since the source documentation is held in a single, secure system that remains unaltered, regardless of corporate reorganizations, divestitures or changes to financial accounting treatments. The platform also provides the necessary analytical and reporting tools to perform complex analyses, automate routine analytical processes, support dashboards, generate scheduled periodic reporting, enable self-service reporting and serve as a system of record for tax compliance reporting. The time saved on data preparation can be used to find the most advantageous ways to allocate revenue and expenses within Pillar Two, for example, by determining optimal transfer prices.

Tax departments also need a dedicated platform that is closely integrated and aligned with the enterprise finance systems because tax data, tax forecasting and tax analytics have separate requirements from other forms of accounting. For example, income taxes are levied at the legal-entity level, which differs from financial or management reporting structures. Tax accounting definitions and treatments are not necessarily the same as those used in financial or management accounting and can differ materially from one jurisdiction to another. In addition, from the taxing authority’s standpoint, tax liability arises within the entity’s fiscal year and is not altered by subsequent events, such as a corporate reorganization or merger. Therefore, it is essential to maintain tax records entity by entity on an as-was basis, along with all inter-period adjustments and true-ups. Having a tax data store of record that is separate from other systems facilitates this and may be the only practical way of meeting this requirement.

We also caution organizations to avoid building their own platform because compared to what is available from a vendor, the time to build and test a comparable system will take longer, the risk of errors is greater, and the total cost of ownership is likely to be higher when all maintenance and update costs are included.

Build a Foundation for Confident and Efficient Tax Reporting and Compliance Today

A dedicated system reduces unproductive data management tasks, giving tax experts more time to devote to what they know best—minimizing tax liability while limiting risk.

ISG Research strongly recommends having a global tax management system with the ability to calculate and translate results to address transfer pricing, tax provisioning and tax transparency obligations like CbCR and Pillar Two. There are three reasons behind this. First, the tax departments will always have several years of detailed, tax aware historical data readily available for analytical and forecasting purposes, immediately facilitating compliance. Second, a dedicated system reduces unproductive data management tasks, giving tax experts more time to devote to what they know best—minimizing tax liability while limiting risk. Third, it allows organizations to anticipate the impact of new tax regimes of any sort and take action in advance of the effective dates because the tax department has the data and the time to evaluate options and chart a course ahead of time so that nobody winds up saying, “I wish we would have…” This evaluation and foresight affect actions such as pricing decisions, supply chain design, make-versus-buy, site locations and staffing, to name a few.

Moreover, even if BEPS and Pillar Two did not exist, such a platform would pay for itself, enabling the tax accounting staff to use their time more effectively, increasing transparency into tax provision and tax positions, simplifying tax audit defense and substantially reducing the risk from spreadsheet errors. It can do so because it can scale to enterprise-wide requirements and enable the department to handle a full range of tasks in a consistent fashion.

Key Takeaways

- BEPS Pillar Two has resulted in an overhaul of the global tax framework throughout much of the developed economies, requiring tax departments in those jurisdictions to evaluate their readiness to manage increasingly complex tax calculations, analysis and compliance.

- Standalone spreadsheets are not effective to handle the increased workloads or ensure compliance and reduce risk. Large volumes of data must be securely collected and maintained, and the use of analytical tools are necessary to help optimize tax expense.

- Utilizing a global tax management application or platform is essential to meet the variety of needs of a more demanding tax reporting environment. Organizations should avoid building their own because existing third-party software is specifically designed for this purpose and is maintained by the vendor. It is likely to have a shorter time-to-value, offer consistently better functionality—especially as new tax legislation is introduced or existing laws are changed—and reduce the risk of non-compliance or paying more tax than necessary.

- A global tax management platform can help build and support a robust and resilient tax department, positioning companies for a streamlined transition whenever new tax rules are implemented as well as enabling analysis and decision-making ahead of the changes to limit the impact on corporate performance and financial standing.

Instilling Confidence in the Era of Pillar Two and Beyond

Multinational Corporations Challenged by New Tax Rules

The Base Erosion and Profit Shifting (BEPS) initiative undertaken by the Organization for Economic Co-operation and Development (OECD) was designed to rein in what has been viewed as excessive tax avoidance by multinational corporations (MNCs). Crucially, the OECD does not have legal authority in this matter but provides recommendations to national governments on how to structure tax codes to address profit shifting by restricting tax avoidance and making international tax rates more equitable. When these recommendations are not universally adopted, it creates statutory patchworks that introduces additional complexity, risk and workloads in corporate tax departments.

ISG Research strongly recommends that tax departments have a third-party dedicated application or platform designed to meet the tax reporting and transparency requirements of MNCs.

Pillar Two establishes a global minimum tax framework through a set of interlocking rules. This structure not only complicates the mechanics of tax determination and provision, it also introduces the need for analysis to determine the best ways to allocate revenue and expenses wherever possible. Moreover, forecasting and analysis are necessary to take taxes into account when making decisions about transfer prices, siting operations, allocating production, choosing investments and determining capital structures as well as all mergers and acquisitions. Yet, as of this writing, Pillar Two will not be adopted by the United States, further complicating matters for tax departments and increasing the value of software to minimize workloads while providing deeper insight into how best to structure tax compliance.

ISG Research strongly recommends that tax departments have a third-party dedicated application or platform designed to meet the tax reporting and transparency requirements of MNCs with the flexibility to provide the specific analysis and reporting capabilities needed by individual organizations. Such a platform incorporates tax-specific logic and enables the department to plan and manage transfer pricing and tax reporting, as well as the specific requirements of Country-by-Country Reporting (CbCR), Pillar Two and any other subsequent tax legislation that introduces higher levels of complexity and scrutiny. A platform also allows the department to easily and consistently manage the data from across the entire enterprise working from a single source of truth. This helps reduce risks caused by data, formula or calculation errors, this provides more time for analysis and contingency planning to optimize tax payments, and it also helps boost the overall efficiency of the department.

Impact of Pillar Two-Type Changes on Tax Department Workloads

Pillar Two has already been adopted in part or in full by all the European Union members, the United Kingdom, Canada, Japan, South Korea and Australia. It has added a further level of complexity to tax calculations, analysis and compliance, increasing tax department workloads such that standalone spreadsheets are no longer an appropriate choice. To ensure compliance while reducing risk, corporate tax departments must be able to: collect and maintain all relevant data, which extends beyond that collected by financial management to include operational and human resources systems; utilize analytical tools to accurately optimize tax expense at the group, jurisdiction and local-entity level while respecting the parent’s risk parameters; and rapidly adjust corporate tax optimization plans and strategies as they update business forecasts country by country, or even at a legal-entity level, to achieve key performance objectives and financial metrics.

Unfortunately, our research found that 59% of organizations with 1,000 or more employees use spreadsheets to manage their taxes. Although spreadsheets are indispensable for many tasks, this manual approach cannot scale to handle the increasing data volumes as the number and complexity of calculations currently in place are exacerbated by Pillar Two. Tax departments must have a dedicated tax data and analytics platform to perform these essential functions. ISG Research advises organizations to find and deploy an alternative to spreadsheets immediately because departments need time to develop best practices for their corporation and translate these into processes that support these practices at the local, regional and headquarters levels.

The Global Tax Management Platform

A key capability of a global tax management platform is automatically gathering all necessary data for tax preparation, compliance, analysis and reporting directly from all systems of record, while enriching and transforming the data where necessary to ensure consistency in ways that satisfy the needs of the department.

Today, manually assembling data consumes a significant amount of time for departments, along with checking and reconciling amounts to ensure accuracy. A platform that automates these processes substantially reduces the risk of errors in data and calculations that may be missed even with careful diligence, especially when facing tight deadlines. This is especially challenging when managing multiple tabs in multiple workbooks with different versions, handled by headquarters and local tax professionals. Our Analytics and Data Benchmark Research finds that 69% of organizations say preparing data is one of the most time-consuming aspects of analyzing data along with 64% that say reviewing data for quality and consistency is also an issue. Pillar Two amplifies the department’s data challenges since it requires that teams collect numbers and information from a broader range of sources, ensures that the data is assembled in a consistent fashion and records the data lineage for audit purposes. And all these additional layers of requirements need to be addressed and satisfied within existing time limits.

A dedicated tax platform retains all the information in an as-was state to facilitate audit defense, especially since the source documentation is held in a single, secure system that remains unaltered, regardless of corporate reorganizations, divestitures or changes to financial accounting treatments. The platform also provides the necessary analytical and reporting tools to perform complex analyses, automate routine analytical processes, support dashboards, generate scheduled periodic reporting, enable self-service reporting and serve as a system of record for tax compliance reporting. The time saved on data preparation can be used to find the most advantageous ways to allocate revenue and expenses within Pillar Two, for example, by determining optimal transfer prices.

Tax departments also need a dedicated platform that is closely integrated and aligned with the enterprise finance systems because tax data, tax forecasting and tax analytics have separate requirements from other forms of accounting. For example, income taxes are levied at the legal-entity level, which differs from financial or management reporting structures. Tax accounting definitions and treatments are not necessarily the same as those used in financial or management accounting and can differ materially from one jurisdiction to another. In addition, from the taxing authority’s standpoint, tax liability arises within the entity’s fiscal year and is not altered by subsequent events, such as a corporate reorganization or merger. Therefore, it is essential to maintain tax records entity by entity on an as-was basis, along with all inter-period adjustments and true-ups. Having a tax data store of record that is separate from other systems facilitates this and may be the only practical way of meeting this requirement.

We also caution organizations to avoid building their own platform because compared to what is available from a vendor, the time to build and test a comparable system will take longer, the risk of errors is greater, and the total cost of ownership is likely to be higher when all maintenance and update costs are included.

Build a Foundation for Confident and Efficient Tax Reporting and Compliance Today

A dedicated system reduces unproductive data management tasks, giving tax experts more time to devote to what they know best—minimizing tax liability while limiting risk.

ISG Research strongly recommends having a global tax management system with the ability to calculate and translate results to address transfer pricing, tax provisioning and tax transparency obligations like CbCR and Pillar Two. There are three reasons behind this. First, the tax departments will always have several years of detailed, tax aware historical data readily available for analytical and forecasting purposes, immediately facilitating compliance. Second, a dedicated system reduces unproductive data management tasks, giving tax experts more time to devote to what they know best—minimizing tax liability while limiting risk. Third, it allows organizations to anticipate the impact of new tax regimes of any sort and take action in advance of the effective dates because the tax department has the data and the time to evaluate options and chart a course ahead of time so that nobody winds up saying, “I wish we would have…” This evaluation and foresight affect actions such as pricing decisions, supply chain design, make-versus-buy, site locations and staffing, to name a few.

Moreover, even if BEPS and Pillar Two did not exist, such a platform would pay for itself, enabling the tax accounting staff to use their time more effectively, increasing transparency into tax provision and tax positions, simplifying tax audit defense and substantially reducing the risk from spreadsheet errors. It can do so because it can scale to enterprise-wide requirements and enable the department to handle a full range of tasks in a consistent fashion.

Key Takeaways

- BEPS Pillar Two has resulted in an overhaul of the global tax framework throughout much of the developed economies, requiring tax departments in those jurisdictions to evaluate their readiness to manage increasingly complex tax calculations, analysis and compliance.

- Standalone spreadsheets are not effective to handle the increased workloads or ensure compliance and reduce risk. Large volumes of data must be securely collected and maintained, and the use of analytical tools are necessary to help optimize tax expense.

- Utilizing a global tax management application or platform is essential to meet the variety of needs of a more demanding tax reporting environment. Organizations should avoid building their own because existing third-party software is specifically designed for this purpose and is maintained by the vendor. It is likely to have a shorter time-to-value, offer consistently better functionality—especially as new tax legislation is introduced or existing laws are changed—and reduce the risk of non-compliance or paying more tax than necessary.

- A global tax management platform can help build and support a robust and resilient tax department, positioning companies for a streamlined transition whenever new tax rules are implemented as well as enabling analysis and decision-making ahead of the changes to limit the impact on corporate performance and financial standing.

Fill out the form to continue reading.